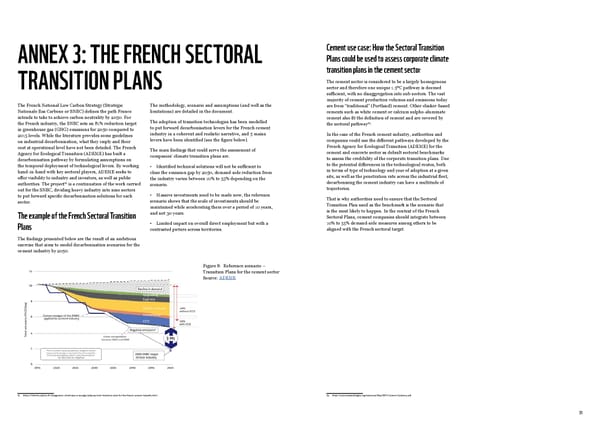

31 61 https://librairie.ademe.fr/changement-climatique-et-energie/5185-sectoral-transition-plan-for-the-french-cement-industry.html. ANNEX 3: THE FRENCH SECTORAL TRANSITION PLANS The French National Low Carbon Strategy (Stratégie Nationale Bas Carbone or SNBC) defines the path France intends to take to achieve carbon neutrality by 2050. For the French industry, the SNBC sets an 81% reduction target in greenhouse gas (GHG) emissions for 2050 compared to 2015 levels. While the literature provides some guidelines on industrial decarbonisation, what they imply and their cost at operational level have not been detailed. The French Agency for Ecological Transition (ADEME) has built a decarbonisation pathway by formulating assumptions on the temporal deployment of technological levers. By working hand-in-hand with key sectoral players, ADEME seeks to offer visibility to industry and investors, as well as public authorities. The project 61 is a continuation of the work carried out for the SNBC, dividing heavy industry into nine sectors to put forward specific decarbonisation solutions for each sector. The example of the French Sectoral Transition Plans The findings presented below are the result of an ambitious exercise that aims to model decarbonisation scenarios for the cement industry by 2050. The methodology, scenario and assumptions (and well as the limitations) are detailed in the document. The adoption of transition technologies has been modelled to put forward decarbonisation levers for the French cement industry in a coherent and realistic narrative, and 5 mains levers have been identified (see the figure below). The main findings that could serve the assessment of companies’ climate transition plans are: • Identified technical solutions will not be sufficient to close the emission gap by 2050, demand-side reduction from the industry varies between 10% to 55% depending on the scenario. • Massive investments need to be made now; the reference scenario shows that the scale of investments should be maintained while accelerating them over a period of 10 years, and not 30 years. • Limited impact on overall direct employment but with a contrasted picture across territories. Cement use case: How the Sectoral Transition Plans could be used to assess corporate climate transition plans in the cement secto r The cement sector is considered to be a largely homogenous sector and therefore one unique 1.5ºC pathway is deemed sufficient, with no disaggregation into sub-sectors. The vast majority of cement production volumes and emissions today are from “traditional” (Portland) cement. Other clinker-based cements such as white cement or calcium sulpho-aluminate cement also fit the definition of cement and are covered by the sectoral pathway 62 . In the case of the French cement industry, authorities and companies could use the different pathways developed by the French Agency for Ecological Transition (ADEME) for the cement and concrete sector as default sectoral benchmarks to assess the credibility of the corporate transition plans. Due to the potential differences in the technological routes, both in terms of type of technology and year of adoption at a given site, as well as the penetration rate across the industrial fleet, decarbonising the cement industry can have a multitude of trajectories. That is why authorities need to ensure that the Sectoral Transition Plan used as the benchmark is the scenario that is the most likely to happen. In the context of the French Sectoral Plans, cement companies should integrate between 10% to 55% demand-side measures among others to be aligned with the French sectoral target. 62 https://sciencebasedtargets.org/resources/files/SBTi-Cement-Guidance.pdf. Figure 8: Reference scenario – Transition Plans for the cement sector Source: ADEME

Corporate Sustainability & Transition Plans Page 15 Page 17

Corporate Sustainability & Transition Plans Page 15 Page 17