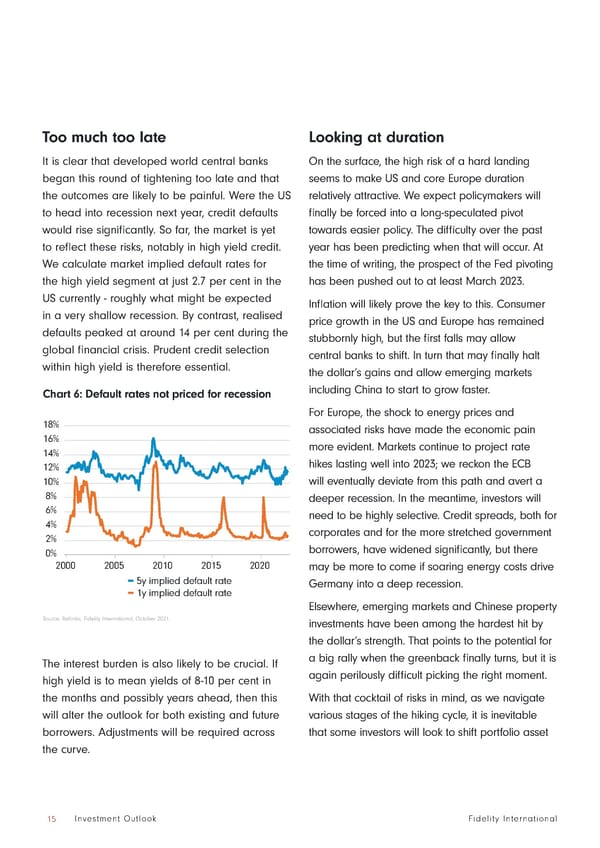

Too much too late Looking at duration It is clear that developed world central banks On the surface, the high risk of a hard landing began this round of tightening too late and that seems to make US and core Europe duration the outcomes are likely to be painful. Were the US relatively attractive. We expect policymakers will to head into recession next year, credit defaults finally be forced into a long-speculated pivot would rise significantly. So far, the market is yet towards easier policy. The difficulty over the past to reflect these risks, notably in high yield credit. year has been predicting when that will occur. At We calculate market implied default rates for the time of writing, the prospect of the Fed pivoting the high yield segment at just 2.7 per cent in the has been pushed out to at least March 2023. US currently - roughly what might be expected Inflation will likely prove the key to this. Consumer in a very shallow recession. By contrast, realised price growth in the US and Europe has remained defaults peaked at around 14 per cent during the stubbornly high, but the first falls may allow global financial crisis. Prudent credit selection central banks to shift. In turn that may finally halt within high yield is therefore essential. the dollar’s gains and allow emerging markets Chart 6: Default rates not priced for recession including China to start to grow faster. For Europe, the shock to energy prices and 18% associated risks have made the economic pain 16% more evident. Markets continue to project rate 14% 12% hikes lasting well into 2023; we reckon the ECB 10% will eventually deviate from this path and avert a 8% deeper recession. In the meantime, investors will 6% need to be highly selective. Credit spreads, both for 4% corporates and for the more stretched government 2% 0% borrowers, have widened significantly, but there 2000 2005 2010 2015 2020 may be more to come if soaring energy costs drive 5y implied default rate Germany into a deep recession. 1y implied default rate Elsewhere, emerging markets and Chinese property Source: Refinitiv, Fidelity International, October 2021. investments have been among the hardest hit by the dollar’s strength. That points to the potential for The interest burden is also likely to be crucial. If a big rally when the greenback finally turns, but it is high yield is to mean yields of 8-10 per cent in again perilously difficult picking the right moment. the months and possibly years ahead, then this With that cocktail of risks in mind, as we navigate will alter the outlook for both existing and future various stages of the hiking cycle, it is inevitable borrowers. Adjustments will be required across that some investors will look to shift portfolio asset the curve. 15 Investment Outlook Fidelity International

Fidelity International Outlook 2023 Page 14 Page 16

Fidelity International Outlook 2023 Page 14 Page 16