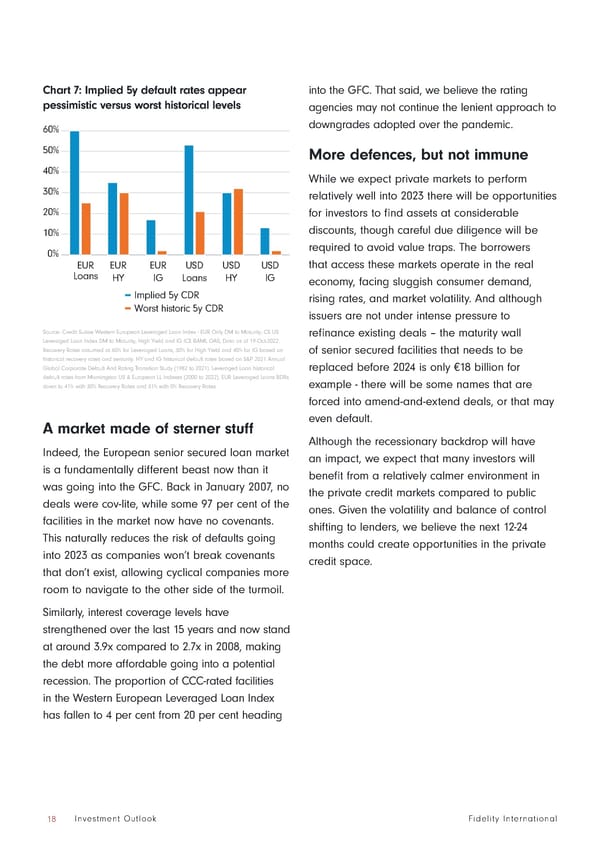

Chart 7: Implied 5y default rates appear into the GFC. That said, we believe the rating pessimistic versus worst historical levels agencies may not continue the lenient approach to 60% downgrades adopted over the pandemic. 50% More defences, but not immune 40% While we expect private markets to perform 30% relatively well into 2023 there will be opportunities 20% for investors to find assets at considerable 10% discounts, though careful due diligence will be 0% required to avoid value traps. The borrowers EUR EUR EUR USD USD USD that access these markets operate in the real Loans HY IG Loans HY IG economy, facing sluggish consumer demand, Implied 5y CDR rising rates, and market volatility. And although Worst historic 5y CDR issuers are not under intense pressure to Source: Credit Suisse Western European Leveraged Loan Index - EUR Only DM to Maturity; CS US refinance existing deals – the maturity wall Leveraged Loan Index DM to Maturity; High Yield and IG ICE BAML OAS; Data as of 19-Oct-2022. Recovery Rates assumed at 60% for Leveraged Loans, 30% for High Yield and 40% for IG based on of senior secured facilities that needs to be historical recovery rates and seniority. HY and IG historical default rates based on S&P 2021 Annual Global Corporate Default And Rating Transition Study (1982 to 2021). Leveraged Loan historical replaced before 2024 is only €18 billion for default rates from Morningstar US & European LL Indexes (2000 to 2022). EUR Leveraged Loans BDRs example - there will be some names that are down to 41% with 30% Recovery Rates and 31% with 0% Recovery Rates. forced into amend-and-extend deals, or that may A market made of sterner stuff even default. Although the recessionary backdrop will have Indeed, the European senior secured loan market an impact, we expect that many investors will is a fundamentally different beast now than it benefit from a relatively calmer environment in was going into the GFC. Back in January 2007, no the private credit markets compared to public deals were cov-lite, while some 97 per cent of the ones. Given the volatility and balance of control facilities in the market now have no covenants. shifting to lenders, we believe the next 12-24 This naturally reduces the risk of defaults going months could create opportunities in the private into 2023 as companies won’t break covenants credit space. that don’t exist, allowing cyclical companies more room to navigate to the other side of the turmoil. Similarly, interest coverage levels have strengthened over the last 15 years and now stand at around 3.9x compared to 2.7x in 2008, making the debt more affordable going into a potential recession. The proportion of CCC-rated facilities in the Western European Leveraged Loan Index has fallen to 4 per cent from 20 per cent heading 18 Investment Outlook Fidelity International

Fidelity International Outlook 2023 Page 17 Page 19

Fidelity International Outlook 2023 Page 17 Page 19