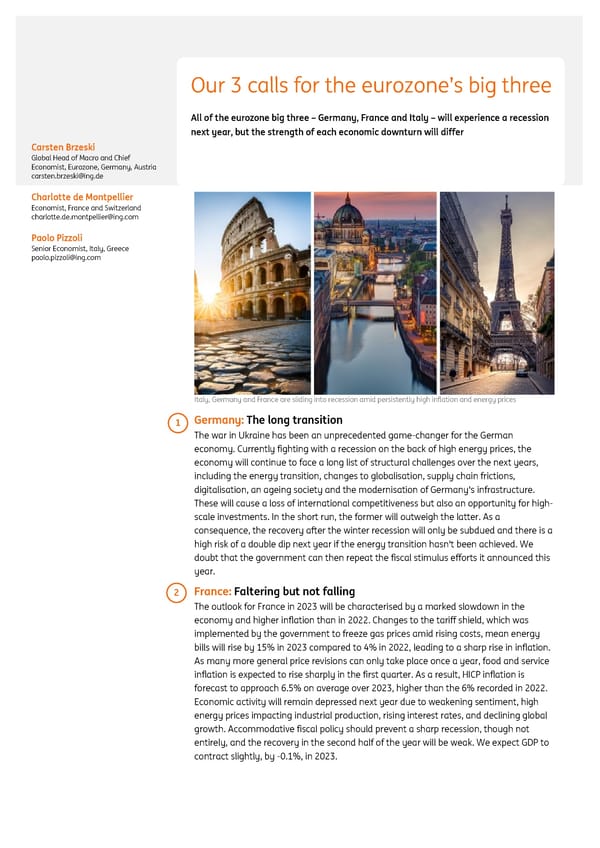

ING global economic outlook 2023 December 2022 Our 3 calls for the eurozone’s big three All of the eurozone big three – Germany, France and Italy – will experience a recession next year, but the strength of each economic downturn will differ Carsten Brzeski Global Head of Macro and Chief Economist, Eurozone, Germany, Austria carsten.brzeski@ing.de Charlotte de Montpellier Economist, France and Switzerland charlotte.de.montpellier@ing.com Paolo Pizzoli Senior Economist, Italy, Greece paolo.pizzoli@ing.com Italy, Germany and France are sliding into recession amid persistently high inflation and energy prices 1 Germany: The long transition The war in Ukraine has been an unprecedented game-changer for the German economy. Currently fighting with a recession on the back of high energy prices, the economy will continue to face a long list of structural challenges over the next years, including the energy transition, changes to globalisation, supply chain frictions, digitalisation, an ageing society and the modernisation of Germany's infrastructure. These will cause a loss of international competitiveness but also an opportunity for high- scale investments. In the short run, the former will outweigh the latter. As a consequence, the recovery after the winter recession will only be subdued and there is a high risk of a double dip next year if the energy transition hasn't been achieved. We doubt that the government can then repeat the fiscal stimulus efforts it announced this year. 2 France: Faltering but not falling The outlook for France in 2023 will be characterised by a marked slowdown in the economy and higher inflation than in 2022. Changes to the tariff shield, which was implemented by the government to freeze gas prices amid rising costs, mean energy bills will rise by 15% in 2023 compared to 4% in 2022, leading to a sharp rise in inflation. As many more general price revisions can only take place once a year, food and service inflation is expected to rise sharply in the first quarter. As a result, HICP inflation is forecast to approach 6.5% on average over 2023, higher than the 6% recorded in 2022. Economic activity will remain depressed next year due to weakening sentiment, high energy prices impacting industrial production, rising interest rates, and declining global growth. Accommodative fiscal policy should prevent a sharp recession, though not entirely, and the recovery in the second half of the year will be weak. We expect GDP to contract slightly, by -0.1%, in 2023.

ING Global Economic Outlook 2023 Page 26 Page 28

ING Global Economic Outlook 2023 Page 26 Page 28