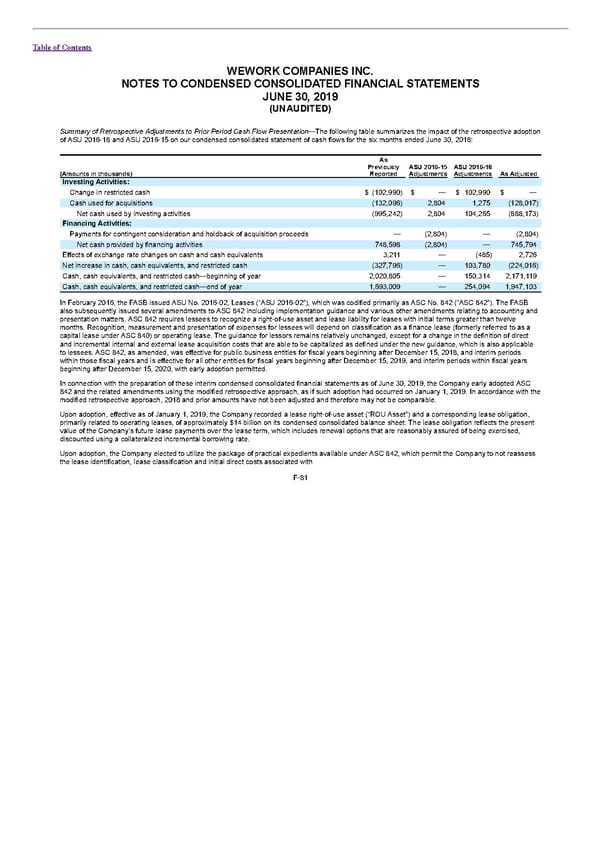

Table of Contents WEWORK COMPANIES INC. NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS JUNE 30, 2019 (UNAUDITED) Summary of Retrospective Adjustments to Prior Period Cash Flow Presentation—The following table summarizes the impact of the retrospective adoption of ASU 2016-18 and ASU 2016-15 on our condensed consolidated statement of cash flows for the six months ended June 30, 2018: As Previously ASU 2016-15 ASU 2016-18 (Amounts in thousands) Reported Adjustments Adjustments As Adjusted Investing Activities: Change in restricted cash $ (102,990) $ — $ 102,990 $ — Cash used for acquisitions (132,096) 2,804 1,275 (128,017) Net cash used by investing activities (995,242) 2,804 104,265 (888,173) Financing Activities: Payments for contingent consideration and holdback of acquisition proceeds — (2,804) — (2,804) Net cash provided by financing activities 748,598 (2,804) — 745,794 Effects of exchange rate changes on cash and cash equivalents 3,211 — (485) 2,726 Net increase in cash, cash equivalents, and restricted cash (327,796) — 103,780 (224,016) Cash, cash equivalents, and restricted cash—beginning of year 2,020,805 — 150,314 2,171,119 Cash, cash equivalents, and restricted cash—end of year 1,693,009 — 254,094 1,947,103 In February 2016, the FASB issued ASU No. 2016-02, Leases (“ASU 2016-02”), which was codified primarily as ASC No. 842 (“ASC 842”). The FASB also subsequently issued several amendments to ASC 842 including implementation guidance and various other amendments relating to accounting and presentation matters. ASC 842 requires lessees to recognize a right-of-use asset and lease liability for leases with initial terms greater than twelve months. Recognition, measurement and presentation of expenses for lessees will depend on classification as a finance lease (formerly referred to as a capital lease under ASC 840) or operating lease. The guidance for lessors remains relatively unchanged, except for a change in the definition of direct and incremental internal and external lease acquisition costs that are able to be capitalized as defined under the new guidance, which is also applicable to lessees. ASC 842, as amended, was effective for public business entities for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years and is effective for all other entities for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020, with early adoption permitted. In connection with the preparation of these interim condensed consolidated financial statements as of June 30, 2019, the Company early adopted ASC 842 and the related amendments using the modified retrospective approach, as if such adoption had occurred on January 1, 2019. In accordance with the modified retrospective approach, 2018 and prior amounts have not been adjusted and therefore may not be comparable. Upon adoption, effective as of January 1, 2019, the Company recorded a lease right-of-use asset (“ROU Asset”) and a corresponding lease obligation, primarily related to operating leases, of approximately $14 billion on its condensed consolidated balance sheet. The lease obligation reflects the present value of the Company’s future lease payments over the lease term, which includes renewal options that are reasonably assured of being exercised, discounted using a collateralized incremental borrowing rate. Upon adoption, the Company elected to utilize the package of practical expedients available under ASC 842, which permit the Company to not reassess the lease identification, lease classification and initial direct costs associated with F-81

S1 - WeWork Prospectus Page 324 Page 326

S1 - WeWork Prospectus Page 324 Page 326