SEOmoz

Prelude: I've long promised blog readers a detailed accounting of my experiences raising capital over the course of last summer and into the fall. My apologies for the long delay, and to those seeking more SEO-focused content. This entry is lengthy, detailed and designed to share as much as possible, so hopefully you've got a good 20 minutes to read it :-) We'll be back to SEO tips & tricks tomorrow.

Sections in this post:

Introduction to our Process & Venture Capital

In this post, my goal is to walk you through the process we used, the feedback we received and the final results and decisions. Fundraising is a demanding, lengthy, emotionally charged process and something that challenged me personally more so than any other single part of my life in the last 5 years. I hope that by sharing my experience I can help others who start down this road and give you an idea of what to expect. The more knowledge you have, the less fear can hold you up; that's what this post is here to accomplish.

First, I'll try to provide some context around why we went to raise money in the first place, how we constructed our "pitch deck," how we got introductions and meetings to a large number of VCs and the progress from initial meetings to partner meetings to final decisions.

SEOmoz started the VC process in June 2009, in possibly the worst climate for fundraising since 2001. You can see the stark contrast from our timing with the previous round in, arguably, the best environment since 2000.

Graph of Venture Capital Invested by Quarter ( via NVCA)

Ventue capital is "expensive" money, not just in terms of the price paid in equity, but in the obligations and requirements that come with it. In our Series A, we took money more like a seed investment - Michelle & Kelly saw potential and wanted to see what could happen. Raising another round meant aiming to hit the "home run." For those who are unfamiliar, the startup world has built an entire lexicon around the "seriousness" and exit-size focus of a company that ranges from "lifestyle" businesses that don't try to achieve multi-million dollar scale to "home runs" that exit for $1billion+.

Note that there's plenty of criticism of this model from both the venture side and from entrepreneurs and operators. Lots of other blogs have talked about the imbalance in interests between founders and investors and current market conditions vs. expected VC portfolio returns. I won't re-hash these, but as a broad overview, most venture funds have 100s of millions of dollars from their LPs (Limited Partners - folks like large endowment funds, pensions, government entities, extremely wealthy individuals, etc). In order to provide significant returns, they follow a model of investing in a few dozen startups, most of which will go bankrupt and, hopefully, 1-3 of which will provide most of the profits in billion dollar+ "exits" (an acquisition or IPO).

This somewhat odd scenario means that VCs are often investing in "long shots" to be huge, rather than low-risk bets for more reasonable exits (for example, an 80% chance of exiting for $150 million is not nearly as interesting as a 10% chance of exiting for $1 billion). As an entrepreneur, particularly a first-time startup guy who has $3,000 in his checking account, an orange scooter and a small apartment, the incentive is completely the reverse. Fred Wilson wrote a bit about this disparity in his post on Swinging for the Fences.

In order to be appealing to a venture investor, especially those with larger fund sizes ($300 million+), a company must be able to show a credible path to that $1 billion+ exit. Since the average VC-backed exit is actually something under $100 million, it's a bit of a "wink, wink; nod, nod" game. Both parties recognize that a more likely outcome is something far lower, but the "sell" has to include the envision-able path to hundreds of millions in annual revenue that can yield those tremendous exits. Again, I'll point to Fred, who wrote about the Venture Capital Math Problem (and a Part 2).

Building the Pitch

You can read a lot more about the catalysts for fundraising on my post - My Startup Experience: VC, Entrepreneurship, Self-Analysis & the Road Ahead - so I'm going to dive right into the process for creating a pitch deck.

We started with a lot of great advice and direction from entrepreneurs who'd been down this road before and also got terrific help from the partners at Ignition, for whom we delivered a "mock" pitch and collected feedback that helped push us in some smart directions. As a base, we used the model promoted by VentureHacks and sprinkled in bits liberally from Dave McClure's excellent How to Pitch a VC deck and Guy Kawasaki's - Perfecting Your Pitch (PDF).

The process itself involved sheets of paper affixed to a large wall, which we'd then swap around, tear up, mark up with pens and generally treat like a post-it-note fight. We started with blank paper that we'd draw on, then began creating real slides in Powerpoint. It was fun - exhilirating and stressful, yes, but also exciting. We were going to raise millions of dollars, put that money to work and build incredible product and an amazing revenue stream.

Before we did that, we had to get beaten up a bit first. I mentioned that we gave a test-run pitch of the deck to the board at Ignition Partners (our first-round investors). We also privately delivered the pitch to a handful of CEOs and angel investors, hoping to garner feedback and assistance (these weren't serious attempts to raise money, as we weren't seeking an angel-type deal). The great part is, we really did get beat up. I have pages and pages of notes from meetings where I showed the pitch to other entrepreneurs and got feedback ranging from "this is almost perfect, just tweak X" to "you need to start completely from scratch, and here's the deck I used to raise $XY millions in my last round."

I'm going to come back to this again below, but the generosity of time, energy and prior work (even stuff that's usually very private) from other startup CEOs and entrepreneurs was absolutely remarkable. I found none of the closed-door mentality or brash indifference I expected, especially in Silicon Valley. Founders and CEOs, who had multi-million dollar businesses to run would take hours out of their days to have lunch, walk through the deck, and introduce us to VCs they knew. I've rarely known so much goodwill from people who have so many demands on their time.

The Pitch Itself

Let's get to the meat and potatoes, as I'm sure by now you're hungry :-)

The "elevator pitch" sounded something like:

SEO is huge - every site on the web is doing it or wants to be. But the process is broken - it's hard to learn, hard to measure, hard to know what's working and far more art than science. We are going to build software that helps transform SEO into a mainstream marketing activity, the way analytics software (Urchin, Omniture, etc.) did for web visitor reporting or email software (iContact, ExactTarget) did for email marketing.

Unfortunately, I'm not going to share the exact deck we used, nor all the details from it. Transparent though I love to be, there's a lot of information and data points that aren't fit for public consumption. It's less that I believe any of this data could be used to materially harm us and more that we've made promises to our investors and board to keep this stuff internal for now. I will say this - while I believed strongly in the deck when we first created it, that confidence was somewhat eroded by the end of the process. In late September, for example, I think I could have done a far better job crafting and delivering the pitch than when I gave my first one in July (only 60 days before).

Below, you'll find a modified version of the original pitch deck (we later crafted many customized versions with slides particular VCs wanted to see). It doesn't include things like a P&L statement or specific customer retention/churn/lifetime value metrics, but hopefully it will still be valuable and interesting.

Since I didn't include revenue/profit numbers in this deck (and it's hard to get a sense for how a potential investor might perceive this without it), I've included some non-specific growth charts below, illlustrating the top-line numbers in a profit-and-loss statement:

I've also left out some portions of our very large appendix. The appendix, in fact, was one of the most interesting parts of the deck. When we started the process, it was 5-6 slides with additional information about market size, importance, some detailed stats on membership, lifetime customer value calculations, etc. A month into the process, it was nearly 30 slides, attacking every question, problem or issue that had been raised in meetings where we didn't have an immediate solid answer or data point. I really believe that the VC process is all backwards in this fashion. The pitching company should:

- Have an introductory call to see if there's interest

- Attend a sit down meeting with a partner or two, some associates and a dilgent notetaker to get all the questions, concerns and issues on the table

- Go back home, make a great deck that addresses the things the VCs care about

- Come back and give the formal pitch

Instead, many pitch meetings at the beginning made us feel like amateurs and it was only at the end of the process that we felt more comfortable tackling any question thrown our way (mostly because we'd heard nearly all of them before). In my opinion, venture capital shouldn't be about who has the most experience pitching, or who can deliver the best pitch, but about who has the most exciting, interesting company. In the current model, it feels like 80% sizzle (pitch) and 20% steak (company).

Then again, what do I know about the VC process? I got lucky in my mid-twenties, landed a bit of capital, and have never invested or even studied the venture model the way the professionals have. Perhaps ability to pitch and success of company are well correlated metrics or at least, indicative of company performance. I'll leave that to those more knowledgable on the topic.

In any case, now that we had this story to tell (the pitch deck), we needed an audience.

Getting Introduced to Venture Capitalists

I initially presumed that our investors (Kelly & Michelle) would drive this process of introductions and networking, but in reality, this is apparently a suboptimal methodology. Michelle explained (and many others concurred) that entrepreneurs themselves provide the best introductions. Thus, it was my task to find other founders & CEOs who would provide positive connections to the investor community. Outside of Ignition, I knew virtually no one in that sphere, so this would be my first formidable challenge.

Thankfully, the entrepreneur community was incredibly kind - generous to a fault, actually. Busy CEOs of important startups took time away from their jobs to sit down for coffee with me, buy me lunch, take me to dinner, review the pitch deck we'd built, give advice and make introductions to a very impressive set of folks in the VC world. In exchange, I did the best I could to help them with SEO, and we hosted a number of great companies at our offices in Seattle for hour-long SEO reviews. It will be hard to thank everyone here, but I'll do my best:

I'm indebted to all of these great folks and I can only hope that the SEO help we provided to many of them has returned some of that.

However, this part of the process is also where we made our first big misstep. Explaining will take a bit of background.

SEOmoz's business model is what's generally called "self-service SaaS." Similar to most SaaS companies, we sell software in a subscription/licensing type of model and, as has become common in the last few years, do it "in the cloud" (meaning we don't install software; everything's run remotely over the web). However, we're very different from traditional "SaaS" in that we have no sales team. There isn't a single person at SEOmoz whose job title or description includes sales (though, technically, if Gillian and I had descriptions, "sales" might be part of that).

Our business model and margins might result in an acquisition price (sale of the company) of between 3-6X trailing revenue, depending on the market circumstances, growth rates, strategic importance, etc. This is massively favorable to consulting revenue, which typically garners 1-1.5X. Put another way:

- An SEO consulting business sale price (assuming $5 million in trailing revenue) = $5-7.5 million

- An SEO self-service SaaS business sale price (assuming $5 million in trailing revenue) = $15-30 million

It's no surprise that investors are far more interested in these "scalable" business models that have higher exit multipliers. This is a big reason why you rarely ever see venture or angel capital flowing into consulting firms. The margins on a consulting business hover between 40-55%. Margins in software get closer to 80%+ and scale isn't proportionally tied to cost (in most consulting businesses, the more you want to make, the more consultants you need to hire).

In our situation, a VC in the B-round would be likely to get something between 15-20% ownership in the company (depending on valuation, amount in, etc). Let's look at a chart that helps explain why we messed up from a strategic standpoint in the introductions process:

Doing the math, even at the high end of the revenue/exit numbers, the VC is making 15% x $450 million = $67.5 million. If you have a $300 million fund and invest in 20 companies, you need at least 6 and hopefully 7-8 of those to hit in that range. The odds say that 10 of those companies will go under, 8 will have much more modest outcomes and 1-2 will return the lion's share. Thus, big fund VCs are going to be seeking portfolio investments that address multi-billion dollar markets and have a shot at that massive IPO/acquisition.

A smart entrepreneur would look at this ahead of time and specifically chase venture capital firms with small-moderate fund sizes. Unfortunately, we didn't plan ahead intelligently on this, and thus talked to many folks with funds between $100-500million. At those levels, it's the 1/20 or 1/50 billion dollar+ exits that bring all the returns for the VC. They're not seeking a reasonable bet on a company that has an long-shot, outside chance at a $500 million exit. They want 20 or 30 companies with 1 in 20 or 1 in 30 chances to go all the way to that billion dollar acquisition or IPO.

Our introductions came streaming in very unstrategically. I met with lots of entreprenuers and people in the tech community, who put me in touch, usually via an email introduction, to a partner at a firm. We'd exchange a couple emails to set up a time to talk, chat for 15-45 minutes (sometimes longer) and then schedule an in-person meeting for the next time I was in their area. Those introductions didn't come all at once - in the first 30 days of actively pursuing introductions, I had ~10 calls. Then, over the next 40 days, more and more introductions would roll in from people I'd connected with in the past couple months, and those would turn into calls and meetings.

I talked to entrepreneurs who were much more strategic and exacting about their introductions process (and plenty who followed a similar pattern to what I did). In hindsight, it wasn't perfect, but I did get to meet a tremendous number of very impressive investors and get their feedback.

The Meeting Process

During our fundraising experience, we connected with a lot of VCs. I've taken a screenshot of the the firms we talked to below (from my Google spreadsheet file on the subject), though I won't go into more detail about who from each firm we talked to or how far along we progressed with each of them. I think there's an expectation of privacy most VCs have, and I want to respect that. BTW - I'm not listing every single firm we talked to, but this is a more-than-representative sample and hopefully fulfills our core value of transparency.

Initially, we were very excited and I'll try to explain why. When starting out, our expectations (thanks to both advice from other entrepreneurs and via blog posts/articles the web) were that 10-20% of phone calls would lead to first meetings , a few of these might turn into partner meetings and we'd hopefully get a term sheet or two at the end. Instead, the funnel looked like this:

As you can see, we had phone calls with 40 firms, and had a surprisingly high conversion rate to first meetings, which had us initially enthusiastic. VCs are notoriously busy, and scheduling time with them is often a massive challenge. To have such a high percentage of firms interested in such a dour climate made us believe we could buck the trend. Unfortunately, it also meant lots of time we needed to invest in preparing for, and in most cases, flying out of Seattle for in-person meetings.

The entire process from the first call I had with a partner (on June 18th) to the time we stopped actively pursuing funding (September 30th) was 93 days. In that time I made 5 separate round trips to San Francisco, which adds up in hotel, airfare and car rentals. Raising money takes time, resources and a tremendous amount of energy, not just from the founder/CEO, but from the entire team. Adam & Matt were consistently pulled away from day-to-day and strategic work to create and refine the product demo. Sarah, Christine & our accountants labored to provide detailed financials. Jeff often had to postpone critical work items to make custom queries against our members database to pull an obscure metric about recitivism, churn or usage.

The meetings themselves are fascinating. I'll be honest - the first few were completely intimidating and overwhelming. Like most times in life when you're nervous, it wasn't until I stopped worrying and (very nearly) stopped caring, that I got good at the process.

You arrive at a nondescript, but very well-adorned office building, almost all of them on Sand Hill Road in Menlo Park. An assistant, who is nearly always young, female, very attractive and somewhat cold (though there were a number of exceptions), greets you in the front room and will offer a beverage. I typically waited only 5-10 minutes, though a few times it was 20 minutes or more, after which I'd be escorted into a meeting room with a place to plug in my laptop to a projector or screen. VC offices provide free wifi (though I always brought my AT&T aircard just in case) and are designed to impress - expensive furnishings and artwork, placards showing the successful companies they've backed and the massive IPOs/exits those companies had.

The VCs themselves ran the gamut, from friendly, approachable and jovial to overly serious, harsh and distant. Intentionally or unintentionally, they all have some emotional walls up, which I believe are out of necessity and certainly don't begrudge. If you're meeting with dozens of entrepreneurs every week, you can't get personally attached or build close relationships with even a fraction of them, especially if you're not going to make an investment. It's a very different experience from the many hundreds of other meetings I've had in my professional career, where establishing rapport and working in a mutually positive fashion is the norm. VCs need to drill down on specifics, call out your flaws, explain what they don't like and gloss over a lot of positives in the process. A typical partner meeting lasts precisely one hour, and in my experience, that rarely deviated (a few times we ran over, and more than a few times things started late).

Second meetings are often pretty similar in format, though there's typically more than one partner from the VC firm in attendance, as well as an associate or two. I also found that it was extremely helpful to bring Sarah Bird (SEOmoz's COO and a guru when it comes to our financials) as well as Nick Gerner and/or Ben Hendrickson (who convincingly play the role of "way smarter about technology than anyone else in the room") to these meetings. They'd sometimes be a bit longer, and would almost always request a much greater degree of detail, as well as significant "objections" to the investment, which were frequently presented as challenges we were intended to conquer using slides, data and verbal acuity.

Following both first and second meetings would be the impossible-to-parse "thanks, we'll be in touch." We'd take guesses about which VCs were actually interested and would follow up vs. those who'd email to say "no thanks" or simply never communicate again (the latter bothered me at first, but once you realize it's just part of the accepted cultural practice, it's fine). Surprisingly, we were never good at this. We'd often mistakenly think one VC was interested when they weren't and vice versa. They're a notoriously hard-to-read bunch, perhaps intentionally.

I have a much tougher time presenting a representative partner meeting, as we only had two. They almost always take place on Monday, though, and you're often back-to-back scheduled with pitches from other entrepreneurs. A larger, board-style meeting room will be filled with all of the firm's partners and you'll present the same pitch you made to the first partner to this group. Questions can get a bit strange if my experience is any guide - tangents and off-topic discussions come into play and it seems to be up to the entrepreneurs to keep things on track. I think this happens because in any given partner meeting, a good number of the partners won't be familiar with your industry, company or technology, and may not even be interested. I imagine that if you specialize in clean-tech investments, listening to an SEOmoz pitch can get a bit boring, and you might, naturally, focus on the one or two areas you know something or have heard something about.

I will say that my experience with the vast majority of VCs we saw was not nearly as negative as what Fred Destin wrote about in his posts for VentureHacks - The Arrogant VC: Why VCs are Disliked by Entrepreneurs and Part 2. Certainly a few of these traits came out, but by and large, I felt these were responsible, talented, experienced individuals doing a hard job the best they could and putting forward both a serious effort and respect for me, my company and my time.

For a completely alternate perspective on what it was like for my wife, who accompanied me on 2 of my 5 fundraising trips, check out A little more than 24 Hours in Palo Alto and San Francisco. I do wholeheartedly recommend someone who loves you unconditionally and pretends to be unable to identify a single flaw in you, your company or your pitch, supporting you in the VC process. It can get very lonely and emotionally turbulent.

What Worked & What Didn't

When it came time to analyze the results, we tried our best to aggregate feedback, both positive and negative, for our board meetings back in Seattle. Early on, we focused on refining the pitch, but we were (I think uncommonly) stubborn about changing our business plan or product roadmap significantly to suite investors' opinions. We felt (and feel) strongly about the direction we want to pursue, and that may have been perceived negatively by some (though I know it was a positive to at least one investor who talked to us afterwards).

Following any "no" response, including a "no answer" within a couple weeks following the meeting, I'd email and ask for a phone call to discuss. 60%+ of the VCs we had met in person took those calls and explained to us some of their reasons for rejecting the investment. I'd specifically ask what they liked, what they didn't and what they recommended for us to improve. I was both impressed and grateful to receive a number of thoughtful, honest answers, and encountered only a couple of folks who clearly didn't remember our pitch or company well enough to provide a cogent response.

Some of the things the VCs generally liked:

- The Self-Service SaaS Business Model - although there were a few dissenters who thought we should pursue a more classic SaaS business with tele-sales would be better, most were supportive of the self-service methodology.

- The Community & Userbase - that's you! Great work, gang :-)

- The Marketing/Sales Funnel - investors tended to like the freemium/content model that attracted potential customers at a low marketing cost

- The Technology Achievements - nearly all of the VCs with technical backgrounds were impressed by what we'd achieved with the Linkscape web index and ranking models work, particularly on such a small amount of capital.

Unfortunately, there wasn't a clear winner in the reasons VCs didn't want to make an investment. I did, however, make a quick chart noting which reasons were most frequently given by the investors for why chose against us:

It's important to note that many of the VCs who said no that we followed up with gave multiple reasons for the decision. Some of these we found very reasonable and agreed with, others we struggled with. The most perturbing by far were the few folks who came back and said they didn't like to back the consulting revenue model and would be more interested once we were more product-focused. When I'd explain that we had 80%+ of revenue for the past three years coming from the self-service SaaS product, awkward silences would follow. Still, these are investors who likely talk to hundreds of companies each year, so it must be incredibly challenging to keep things straight - and it speaks to our need to move away from consulting in our branding and perception.

The Final Outcome

It's likely very obvious at this point that we didn't receive term sheets or offers to fund. In actuality, that's not technically the case - we did have firms interested, just not a the relatively high pre-money valuation numbers we sought. As you can see in the graphic above, there were a number of VCs who may have offered us terms at a lower valuation, though it's hard to say for certain.

The reason we went in with a high valuation "ask" goes back to the very beginning of the post. From the founders' perspective (and those of employee shareholders), an exit has to be judged through the lens of ownership percentages. If I or Gillian or Sarah owned, for example 50% of SEOmoz's shares (none of us do - this is just an example), in a $20 million exit, we'd make $10 million. If venture capital comes in and dilutes that to 35% ownership, that number drops to $7 million in the same exit scenario. Hence, every owner of SEOmoz shares has a vested interest in seeing the final exit price reach the highest possible figure while maintaining the lowest possible level of dilution.

My understanding is that it's very unorthodox to present a minimum pre-money valuation to investors prior to a term sheet. I believe this is because you're potentially "laying too many cards on the table" and you may actually be hurting yourself if the VCs planned to offer a higher pre-money figure. We did it both because we like to be transparent and because we hoped to prevent ourselves from wasting time with investors who couldn't meet our minimums. Our hope was that by giving that number in the first conversation (over the phone) and in the initial pitch deck, we'd achieve similar results as those we had in the past by publishing our prices for consulting - reduce the target market size and improve the quality.

I tell this story about our VC experience to a lot of people - it seems to be a subject that attracts great curiousity and I, of course, love to share. Most of the time, folks follow up by asking "are you disappointed?" and my answer has been the same since October. I'm not disappointed we didn't get funded. In fact, the more time passes and the more I think about the pitfalls that could have come with another round of investment, additional board members and pressure to reach $75-$100 million in annual revenue, the more I'm glad we didn't. However, I do regret the decision to seek funding - it cost our team countless days and weeks of productivity, took our eyes off our primary goal of delighting our members and customers and, in the end, was a learning experience with a shockingly high cost.

That said, I do think we learned a tremendous amount and really helped clarify the vision internally and to our existing board members and investors about where this company is going and what our roadmap looks like. We had dozens of smart, analytical, experienced investors reviewing our plans and ideas, and we received a lot of very positive feedback. Nearly everyone we encountered had positive things to say about the business' future, regardless of investment, and I'm glad we were able to be in a situation where we could turn venture funding down. I have friends here in Seattle and in the Bay Area who didn't have that luxury - who HAD to get funded, no matter the cost, because their company's future and employees depended on it. That's a burden I don't wish on anyone, and I hope more and more startups are finding ways to live lean and do more with less.

So, it's 3:45am and I've been working on this post on and off since before the holidays. There's so much more I want to add, but I think I'll leave that up to you. If you have questions I can answer, PLEASE post them in the comments and I'll do my best to incorporate that material into the post as it makes sense. Thanks for all the support, kindness and patience - I hope this has been valuable.

p.s. In Summer 2011, we once again were seduced by the promise of outside investment and had another not-so-great experience with VC funding you can read here.

The Next Stage of Moz: How a tiny Mom + Son consultancy became the world leader in SEO Software, and our roadmap to being Seattle’s next $1 Billion company Rand Fishkin, CEO& Co-founder, SEOmoz July 2011

Did you know? At one point, Rand + Gillian had just under $500K in personal debt. By 2007, it was all paid off, thanks to the magical super-awesomeness of SEO! 2004 1981 1997 2001Feb. 2007 Nov. 2007 Oct. 2008 Sept. 2010 July 2011 Gillian (Rand’s Mom) founds the company that will become SEOmoz Rand starts working w/ Gillian building websites for small, local businesses Rand drops out of UW, 2 classes from graduation to work full time w/ Gillian Deeply in debt, and failing to get traffic to clients’ sites, Rand starts the SEOmoz Blog as part of learning the SEO process. SEOmoz launches its first subscription software product, “PRO” for $39/month SEOmoz takes an investment of $1.1M from Ignition Partners & Curious Office Linkscape, SEOmoz’sweb index and link graph, launches. By December, mozis profitable. A Little MozHistory (now in color! ) Moz’scollection of tools becomes a singular, campaign-based web app. Prices rise to $99 / $499 / $1999 per month. SEOmozis moving from just “SEO” to social media, content marketing, analytics, local and video. To this end, we’ve acquired “Moz.com.”

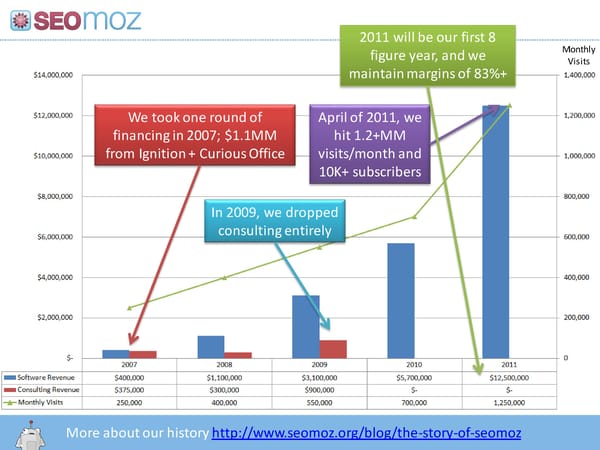

More about our history http://www.seomoz.org/blog/the-story-of-seomoz Monthly Visits We took one round of financing in 2007; $1.1MM from Ignition + Curious Office In 2009, we dropped consulting entirely April of 2011, we hit 1.2+MM visits/month and 10K+ subscribers 2011 will be our first 8 figure year, and we maintain margins of 83%+

How’d We Do That?

Up until 2010, SEOmoz had never spent money directly to acquire customers! (No PPC, no ads, just conferences and content production, aka “sweat marketing”) Blogs + Blogging Comment Marketing News/Media/PR SEO Social Networks Word of Mouth Q+A Sites Forums Online Video Podcasting Webinars Research/White Papers Infographics Social Bookmarking INBOUND MARKETING! (AKA all the “free” traffic sources) Direct/Referring Links Type-In Traffic Email Local Portals

That’s what we want to help other companies measure + improve through our cloud-based software.

Macroeconomic Trends that Benefit Moz

Via http://www.ftijournal.com/images/uploads/Journal _p6-7 .pdf Marketing Spend is Still Unbalanced vs. Behavior

Organic Marketing is Under-Invested Web Traffic is driven almost entirely by organic/earned media, yet nearly all of the investment in driving traffic to websites is through paid channels… This is an unsustainable dichotomy. Organic drives 90%+ of traffic (but garners only ~$5 billion of investment in 2011) Paid drives <10% of web traffic (but wins a whopping $31+ Billion of investment in 2011) Percent of W eb Traffic from Various Sources to the Average W ebsite

These challenges require scalable, high quality software to solve. Very few companies are investing in this space in a serious way, and almost none target the SMB market. It’s a Data-Driven World and Efficiency is King

Problem(s) We’re Here to Solve

Organic Web Marketing is Poorly Understood Even those marketers who have an understanding of the process often get lost in the details or mired in the complexity of tying creative to metrics. Invest in Content, Search, Social, Local and/or Participatory Online Channels Measure Traffic and ROI Effectively Re-Invest in ROI- Positive Channels Earn Outsized Traffic/Branding/Customer Acquisition Rewards vs. Paid Marketing Channels

The Web Marketer’s Weekly Analytics Challenge FacebookInsights Twitter (Topsy/Hootsuite) Every week (sometimes daily), web marketers need to log in to each of these services (or a suitable substitute) to collect their KPIs: FourSquare Yelp Google Analytics Google Webmaster Tools Bing Webmaster Tools Google Alerts Google Local Many (75%+):Most (~50%):Some (~10%): SEOmoz Feedburner PostRank Why should a marketer log into 10+ sites/tools just to get the basic numbers they need to measure and improve their campaigns? Mozcan (and should) put this all in one place. Bit.ly Yahoo! Site Explorer

Specific, Painful Web Marketing Tasks Each of these requires special tools, large amounts of manual labor or custom-built, in-house/agency solutions: Researching New Opportunities Identifying High- ROI Channels Prioritizing + Managing Tasks Finding Errors + Problems Optimizing Existing Channels Training New Marketers These challenges require scalable, high quality software to solve. Very few companies are investing in this space in a serious way, and almost none target the SMB market.

Our Target Market

Today, Mozfocuses on just the red “SEO” circles. In the future, many more of these will become customer targets. (BTW -I cheated by using two bubbles for “SEO” –sorry about that Venn Diagram purists!) Mozhas captured an estimated 5-10% of just these 2 circles to date

We Help Marketers Who Focus on Organic We believe we’ve captured ~5% of this market as paying customers and ~15% as registered members

Immediate Customer Targets: SEO Specialist Search Marketer These titles/job functions represent our current (2011-13) targets: Site Owner Domainer Director of Marketing Online Marketing Manager SEO Consultant Organic Marketing Consultant Webmaster In-House (~55% of current members) Consultant/Agency (~35% of current members) Independent (~10% of current members) Blogger Search + Social Consultant Social Media Expert These job titles/functions have the most direct use for our current software subscription. Web Marketing Consultant Director of Growth Inbound Marketer

Where are We Today?

Number of PRO Subscribers # of New Free Trials / Day Implied Customer Life Avg. Customer Lifetime Value Avg. Cost of Paid Acquisition 2011 Estimated Revenue Current Revenue Run Rate (June) ~13,500 ~100 ~9 Months ~$900 ~$100 $12 -$13 million ~$10.8 million Avg. Monthly Revenue / Subscriber~$93

Monthly Visits to Moz+ OSE Email Subscribers Estimated Net Profit in 2011 Gross Margins Staffing Costs % of Free Trials Converting to Paid Churn Rate in 1st2 Paid Months ~1.25 million ~300K ~$1 million ~82% ~$650K / Month ~57% ~25% Crawling, Serving, Hosting + Processing~$180K / Month

Planned Investment Round

Onto Balance Sheet: New Board: Raising: Founder Equity: $13-19 Million 2 Investors (Michelle +1) 2 Insiders (Rand +1) 1 Independent (TBD) $20-$25 Million $6-7 Million

Business Risks

Google Integrates Much More SEO & Social Analytics Functionality in the Short Term

The Web Becomes Less Open

We Fail to Adapt/Grow Fast Enough to Keep Up w/ Organic Marketing Shifts

Our Reputation Suffers Due to Missteps in Culture, Data Quality or Reliability

Use of Funds / Growth Opportunities 2011-2012

Serve a Wider Audience w/ Expanded Product Whatever organic marketers are using to drive traffic and derive value, we’ll help them measure, monitor and improve it with a suite that ’s simple enough for anyone but powerful enough to support advanced-expert level practitioners. Become the Default Productivity + Research Suite for Organic Web Marketers

2 Year Team Roadmap from 40-100 Mozzers User Experience Product (Design the Right Software) Design + UI Subject Matter Experts Wireframing+ Specs Testing / QA PR / Press / Outreach Paid Acquisition Broad Web Crawl Rankings Data Events Engineering (Build Amazing $#*!) Marketing (Bring in Customers) Content/Media/Research Local Data Community Management Social Data Front End / Web App Fresh Web Data Operations (Make MozRun Smoothly) Customer Success (Delight MozMembers) Retention (Keep PRO Members PRO) Quant + Cohort Analysis Email + On-Site Messaging Q&A Assistance API & Higher-Tier Sales Customer Service Customer Outreach Financial + Accounting Facilities HR/MozzerHappiness

Over the course of this year, I've written a couple times about raising a potential round of venture financing for my company, SEOmoz. At last, the saga's over, I've been released from terms of confidentiality and I can share the long, strange story of how I first rejected, was eventually persuaded, but ultimately failed to raise a second round of investment capital.

photo creditDo We Really Want to Raise a Round?

My hope is that by sharing, others can learn from our experience and possibly avoid some of the mistakes, pitfalls and pain we faced.

Raising money for a startup is an inherently risky proposition. You step up to the plate knowing that the odds are slim and that, for every story of success on TechCrunch, there's two hundred companies pounding the street, getting nowhere. We went the opposite route - letting investors come to us (a strategy I wrote about last year). This is the story of that experience - being "pitched" by investors, the decision-making and negotiation processes and the end results.

In November of last year, 14 months after my previous failed attempt to raise capital, we started receiving inquiries from a variety of firms - venture capitalists and private/growth equity investors, asking if SEOmoz was interested in pursuing funding. My answer was always the same, and looked fairly similar to the email below:

Over the following months (Nov 2010 - April 2011) we hunkered down, focused on product, technology and marketing and grew the business, largely ignoring the possibility of outside funding.

In March of 2011, one particular investor (whom I'll refer to through the rest of this post as "Neil") reached out to us and was especially excited about the SEO/inbound marketing sector and SEOmoz in particular. He sent this email after our call:

It was flattering and exciting to feel this great level of interest in our business from an investor, and Neil wasn't the only one, either. Here's a list of the folks we talked to seriously (meaning more than just a single phone call or email) over the first 7 months of 2011:

* Bessemer Venture Partners

* GRP Partners

* Stripes Group

* Insight Ventures

* JMI Equity

* Level Equity

* Mayfield Capital

* Accel Partners

* Summit Partners

* NEA

* General Catalyst

* K1

* Industry Ventures

For the firms noted above, I'll keep specifics of who we spoke to and how far we progressed private (as I did in my post on the 2009 experience) using pseudonyms.

The week of May 8th, I met with 3 investors in New York City and one in Boston. In preparation for these meetings, I tried to remind myself that money might not be the best thing for the company with a public blog post on the topic. I was focused on the goals of building relationships, sharing our trajectory and learning as much as possible about how others viewed our business and market.

Despite this bevvy of interest, my previous fundraising experience had left me gun-shy and reticent about committing. A week after the meetings in NYC, the Moz team had a serious chat about whether raising a round could have a serious, positive impact on the company. That discussion included a lot of back-and-forth, but the reasons we ultimately decided to test the waters more seriously included:

* Grow Engineering - For the first quarter of 2010, we had a mandate to grow the engineering team so we could improve our product faster. This proved incredibly difficult, as the much-reported tech talent wars in Seattle created a vacuum of big-data savvy SDEs. However, in Q2, our position shifted as we were able to significantly grow the engineering team - to a point where we had to slow hiring in order to keep payroll in line with our bootstrapped growth. While certainly a positive, this change meant that we were limited by cash in the bank for the first time in a while.

* Scale Data - Linkscape, Blogscape and our APIs cost ~$100K/month at the beginning of the year. In Q2, this cost had risen 30%+ and we foresaw a nearby time when it would double or more. In July of this year, those costs were, indeed, nearly $200K. We've gone from 40 virtual machines hosted on Amazon to 200+, and while we're thrilled to see our metrics (mozRank, Domain Authority, et al) achieve widespread adoption, many of the heavy users employ our free API, leaving our revenue from other channels to support these costs. Long-term, we believe in free, open data as a way to grow the brand, the company and our revenue-producing channels (and it's part of our core values to be as open and generous as possible with our data), but the cash limitations had finally become a point of frustration, and another reason to seek growth capital.

* Expand Facilities/Benefits/Team Happiness - The Moz offices can comfortably hold 45-50 people, but we realized that by Q3, we'd already be at that range. We also recognized that the aforementioned talent wars were pushing us to grow the range of benefits and space we provide to the team. Moz was named #6 on Seattle's Best Places to Work, but we're striving for #1, and we strongly believe that the better we can treat our team, the more amazing our output and results will be.

* Release New Products - Our big data projects have been challenging, but also incredibly rewarding, and we felt a strong drive to do more, faster. We want to produce marketing analytics beyond pure SEO, moving to field like social, content marketing, local and verticals (mobile, video, blogs, etc. - anything that sends traffic on the web organically). Some of those require heavy upfront investments in data sources, engineering and market research. One of the weird things I've found (which probably deserves a post of its own at some point) is that the larger your scale, the longer it takes to build product. You'd think that having 15 full-time engineers and a significant support team around them would mean faster development, but it doesn't - the scale we need to support (nearly 14K paying customers and 250K+ users of our free products) for anything we release means far greater attention to architecture, reliability and quality then when we had two devs and 500 users.

* Invest in Marketing - Today, most of SEOmoz's acquisition of new customers is through inbound/organic channels (~80%). We recognize there's a lot of room for growth in both organic (content marketing, more community investment, SEO, social, etc) and in paid marketing. An investment here would allow us to take a longer view on customer payback period (the time until we recoup an investment in acquisition) and experiment in new channels, too.

Testing the Waters for a Large Financing Round...* Provide Liquidity to Founders - Gillian founded the company that would become SEOmoz in 1981 and I've been working with her since 2001. As Gillian's stepped aside from day-to-day responsibilities (post 2008) and taken on more of an external evangelism role, we all felt that giving her a more formal exit and liquidation path would be an ideal option. I also personally felt it was wise to take some money off the table.

I'd be remiss if I didn't also mention another meeting in Boston - with Hubspot's Dharmesh Shah. For the past few years, Dharmesh has been an amazing mentor to me, and someone whom I always turn to when big decisions like this appear. On the topic of funding, he gave clear, well-reasoned advice (and later, made that advice public). We met in May, just after my in-person meetings in New York, and noted that the combination of a great market for investment plus strong growth at the company made for excellent fundraising conditions.

Thus, in mid-May, when Neil asked to follow up with an in-person visit to our offices in Seattle, I sent the following email reply:

After that meeting in Seattle, things got hot and heavy. Neil wanted to do a deal and we began talking terms. It was at this point that our executive team and board of directors decided to take some steps to insure that we were making the right moves. These included:

* Meeting with and, hopefully, receiving offers from 2-3 of the other firms who had reached out to Moz to help test the waters on valuation and deal terms, and to make sure we had a partner and investor we loved.

* Deep-diving on Neil and his firm. We ended up speaking directly to folks at 2 of their portfolio companies, several people who worked with Neil in his previous roles and back-channeling to nearly half a dozen others who'd worked with him in one way or another through our network of contacts (both at Moz, and through Ignition Partners, our investors from 2007).

* Working hard on long-term, strategic planning for 2012 and beyond - what did we want to do, how much would it take, and where would the money be spent?

* Preparing a semi-formal slide deck to pitch the partnership at Ignition, as we wanted them to participate in the round as well. We also made a light version of this deck to send around to several folks in the field and help drum up any potential interest without being too forward or pushy.

* Investigating the fundraising market for self-service SaaS companies like ours by talking to as many recently funded entrepreneurs in the space as possible. Through this research, we hoped to get a good idea of what sorts of terms and valuation we should expect, and what was "market" (VC-speak for "normal").

Narrowing Down the FieldIn mid-June, I made a trip to San Francisco, ostensibly to participate in SimplyHired's SEO Meetup, but also for several Bay-Area meetings with VCs. Three of these turned into more serious discussions.

June was also when we started to feel a bit cocky. We were in active negotiations with Neil. We had multiple talks going with investors in the Bay Area, and almost every week, we had a ping from a new source reaching out to see if we were ready to start a conversation. I spoke to dozens of folks by phone and email and learned a lot more about the market - and those conversations gave me a lot of reasons to get excited. As in 2007, a lot of startups were reporting a very hot market for raising money. Valuations of several SaaS businesses I talked with were in the 6-10X revenue range (and those who raised in Q1/Q2 got valued on their 2011 estimated revenues)!

Throughout the process, we'd been extra careful on the investors we engaged. We turned away one firm due to a bad experience we had with them in 2009 (email below).

This example wasn't alone - we turned away another after talking to some of their portfolio companies and a company they'd look at but didn't invest in and hearing about some questionable behavior.

Our biggest filter wasn't deal terms or price, but cultural fit. We'd been warned many times against adding an investor who didn't share our core values or who displayed any dishonest/manipulative tactics in our conversations. That ruled out a few folks, but also made us more excited about Neil, "Reggie" (an investor in California) and "Todd" (at another California-based firm).

One of my favorite emails in our process came from Reggie, who sent this just before their in-person visit to the Mozplex:

Adorable, right?! Sometimes, it's the little stuff. Neil always asked about my grandmother in New Jersey (she had a rough fall, a concussion and spent a few weeks in hospitals, but is now nearly 100% and doing well). Todd wolfed down multiple helpings of phenomenal braised pork shoulder made by our systems engineer, David. Sarah and I dragged both Neil and Reggie to meals with both of our significant others.

But, the fundraising process certainly wasn't all fun, and it did require a tremendous amount of work, particularly from Sarah, Moz's COO, and from Jamie + Joanna on our marketing team, who held numerous calls with investors on a ton of membership acquisition/retention-related topics. Here's a brief snippet of a weekend email thread that Sarah sent to Todd:

Closing the DealIn June and July, the funding process probably entailed hundreds of combined hours of work on the part of our team - much of that was me, but plenty spread to other departments and functions. We knew this was a very big decision - one that would massively impact the future of the company - and thus, we wanted to be as diligent, thoughtful and cautious as possible.

By early July, we were down to four potentially serious investors. One decided against making an offer around the middle of the month. The others were Neil (from NY), Reggie (from CA) and Todd (also CA).

At the beginning of July, one of the investors made an offer at a $50mm pre-money valuation for a $25mm investment. Here's my email reply:

That offer was subsequently raised to $65mm pre-money, which was matched by another firm (both Neil + Reggie). I was feeling pretty good about my negotiation skills, until a couple weeks later.

Todd was an early favorite of several Mozzers. At the end of his visit to our offices, I gave him a ride back to the airport (I borrowed Geraldine 's only-slightly-dented 2003 Kia Spectra, since I don't actually own a car). Near the end of the conversation, Todd noted that his firm "would have a tough time getting to $100mm" on our deal. I probably should have corrected him at that point (it would have been the TAGFEE thing to do), but I instead said something like "this isn't entirely about the highest pre-money valuation; it's about the right fit for us." This would serve as a good example of why I shouldn't try to "play the game." A week later, after lots of back-and-forth, Todd noted that his firm simply couldn't match our valuation expectations, and although interested, would be backing out.

Pitching Ignition PartnersI'm not sure if our strategy with Todd was a big misstep or a small one, nor whether they would have made an offer in the $60-$70mm range if they'd thought that was our target. I also don't know why he thought we were offered those much higher numbers, nor what we should have done from there. We could have gone back and pushed on what they thought we wanted, but it seemed the time had passed (hard to describe why/how exactly).

We made our decision, sent a polite note to Reggie thanking him and another to Neil saying we were ready to move.

In addition to raising funds from an outside partner, we also wanted Ignition, who had put $1mm into the company in 2007 to participate in this next round. Their support would be helpful in making outside investors feel great about the deal, and would help us have more shared ownership among our board members.

Below is the pitch deck I used for Ignition (parts of this made it into the "light" version we sent to some other folks earlier in the process):

Note the delicious-looking baked goods on the table

Note the delicious-looking baked goods on the table

We've had a terrific relationship with Ignition over the years, and I continue to recommend them to startups of all kinds. As part of the "thank-you" for their support, Geraldine baked some cookie bars the night before our pitch meeting, which I brought to their offices and handed out prior to the presentation. I took a photo hoping that I'd be able to share it on the blog once the deal was done:

Ignition confirmed, just after this meeting, that they'd love to participate in our next round, in whatever quantity made sense to the outside, lead investor. We were excited, and spent some serious time in July planning a comprehensive strategy around how to grow with the funding. We even started some conversations with other companies we were considering acquiring.

Neil brought several folks from his firm to our annual Mozcon in Seattle. On the last afternoon, we met to negotiate some final terms of the deal. It ended up looking like this:

Then Things Got a Little Weird* $24mm invested; $19mm from Neil and $5mm from Ignition

* $65mm pre-money valuation, $89mm post

* $18mm to SEOmoz's balance sheet; $4.75mm to Gillian, $1.25mm to Rand

* No liquidation preference for Series B (Ignition has a 1X on the Series A)

* Straight preferred (meaning that the investor either gets their money out in a sale OR the percent of the company they own, but not both)

* New board would include myself and Sarah (our COO), Michelle (from Ignition, who's been on our board since 2007) & Neil plus a new, outside member to be approved by all parties

* The CEO could only be replaced if ALL board members unanimously approved the new person

* A sale of the company for less than a 3X return to Neil's firm could be vetoed by them

* All other terms very similar to our Series A deal

We felt really good around these terms, and although we recognized we likely could have gotten a higher pre-money valuation through a more intensive process, we decided not to take that path, reasoning that delay could cause a dip in the markets, and that we needed to concentrate on the business, not spend more time on fundraising.

On August 5th, we executed and entered a 30-day due diligence phase.

Michelle was the first to note that something was "odd." In a phone call with Neil, she heard him comment that they "needed to do more digging into the market." In her opinion, this was very peculiar, as investors typically have a thesis and great quantities of diligence long before talking to companies, nevermind prior to a signed agreement. In fact, when Neil approached us, it had been under the auspices of excitement about the SEO/inbound marketing field. One of the things we liked best about them had been their strong belief, passion and knowledge about the SEO landscape. Questions about "market size" and "opportunity" at this stage seemed peculiar.

I shot Neil an email noting that we were a bit concerned. Here's his reply:

We didn't actually chat that night, but a few days later. On the call, he strongly disabused me of the idea that they'd pull out, noting that they had invested massive time and energy, multiple trips to Seattle, multiple people from their firm, considerable research and expense. One of the most memorable quotes from that conversation that stands out in my mind was "We never pull out after signing an LOI unless we find fraud or some other serious misrepresentation of what we already know."

We set up a lunch date for the next week on a Friday, just prior to their planned, in-person diligence with our team the following Monday/Tuesday (when their legal, accounting and tech folks would be meeting with teams and execs to make sure all was in order).

One other item Neil mentioned in the call was our July numbers - we'd just closed out the month and sent them details a couple days prior. Neil noted that they were curious about why July's revenue was off budget by ~$70K. I promised to follow up and provide details.

For reference, here's our revenue numbers from January to July of 2011:

In December, our draft budget had us doing approximately $15K more in revenue in June and $70K more in revenue (both product - our only services revenue is events like Mozcon). However, we'd beaten revenue estimates from January - May and thus, were still ahead of our total revenue target by ~$35K for the year.

Nonetheless, given that June and July were slightly slower in growth of new PRO members (we grew approx. 7% in July vs. our projected 10%), Sarah revised our rolling forecast for the year, projecting that rather than hit $12.4mm (our previous rolling forecast given our higher-than-expected growth Jan-May), we'd instead be around $11.2mm unless growth in future months picked up again. Our model for the rolling forecast is fairly standard and fluctuations like this are fairly common. At one point earlier this year, the rolling forecast had us projecting nearly $14mm, and as low as $11mm.

Ugh. Bad journalism.

Ugh. Bad journalism.We didn't worry much about these numbers - for the past 4 years running SEOmoz, we've often see months that beat our targets and some that don't. Certainly, a month where we expected 10% growth but only hit 7% was nothing shocking, particularly in a year where, even with the revised estimate, we'd be doubling revenue from 2010 (in which we did $5.7mm).

Unfortunately, our new would-be-investors didn't see things that way. Well... Maybe.

The following week (Tuesday, August 16th), VentureBeat wrote a story that SEOmoz had closed a $25mm funding. I quickly commented on the story and called the reporter. They fixed the piece a few hours later:

I also got on the phone with Neil, but he didn't seem overly concerned about the misinformation or the story. As far as I know, no one at Moz was responsible, and the misinformation made this seem incredibly unlikely. Given the numerous inaccuracies (our employee count, customer numbers, the description of what we do and more), I really have no idea who their source was, or why they published this piece without waiting for our confirmation or statement.

We went back to work on the diligence documents and preparation, a bit shaken and more than a little skeptical.

Two days later, the day before Neil and I were to meet for lunch, he sent an email indicating they were cancelling their in-person diligence in Seattle (planned for the following Monday/Tuesday) pending our meeting. I immediately assumed they were killing the deal, and emailed the Moz team to stop the work for the process on our end.

We met in New York and had lunch. I took notes:

I thought they were going to focus primarily on the growth we missed in July - despite knowing that it wasn't a big deal from the long-term perspective of the business, it was nerve-wracking and hard-to-shake in those few days. But instead, we talked for nearly 2.5 hours about our market strategy, how we planned to expand our product, deliver more value, etc. Neil shared a lot of what they'd learned talking to CMOs, VPs of Marketing and SEO specialists at companies they knew. It was all pretty flattering, actually - I was shocked at how positive the feedback had been.

The only big concern he brought up from that research was that higher-up marketing executives still lack belief in SEO. One quote that I noted above was a VP who said "I know it's irrational, but nobody can prove to me that we should spend more." This lack of investment in SEO and inbound marketing compared to paid channels, despite the higher ROI and lower acquisition cost, is something every inbound professional fights against.

At the tail end of the conversation, Neil brought up their concerns around our July numbers. They asked whether we felt the month was "a blip or a softening of the market." I explained that when we looked into it, we saw a few major drivers:

* June/July lacked major new product releases/improvements as we geared up for MozCon at the end of the month (where we had three big releases, including the new OpenSiteExplorer, one of our flagship products)

* We had turned off re-targeting ads for SEOmoz and OSE in late June as we switched providers and didn't have it on again until early August. Re-targeting's great for us, because we have such high organic traffic, and it brings those visitors back. Based on the May/June numbers, we likely lost between 5-10% of new memberships from this alone.

* May, June and July also didn't feature as many upgrades and improvements to our performance marketing channels, primarily because we focused the team's time on other projects, including, notably, calls, metrics requests and data dives related to fund raising.

Why Did The Deal Fall Apart?* We put more attention and effort than intended on events - Mozcon and our Mozcations - and less on our funnel. We were definitely feeling a bit cocky thanks to our better-than-expected January-May.

* The team was distracted by fundraising. I actually didn't use this explanation when talking to Neil (I think I felt ashamed of bringing it up - that it would make us look worse than the others), but it certainly played a part.

I also told Neil that, if it was very important to them, we could certainly hit the $12.4mm revenue target for the end of the year by focusing on short-term acquisition, but that it would come at the expense of longer-term projects, and we felt that was unwise and unwarranted.

The meeting wrapped up, and Neil promised me an update by Monday. Tuesday morning we got the call; no deal. They released us from the term sheet conditions including, generously, the associated NDA. I promised that in the blog post I'd write (the one you're reading now), we'd keep their identity anonymous, "Dragnet-style."

We have a few working theories, but don't know for sure.

* What Neil Told Us - according to Neil, the sole reason for their exit was the softness in the June/July numbers. However, this is very hard for me to swallow. We literally missed growth in two months where we had a combined $1.8mm in revenue by $85K, and we were still technically ahead on the revenue projections for the year (by $35K).

* The VentureBeat Theory - one guess is that someone important and trusted by Neil contacted him following the VentureBeat story and advised them not to put money into us for one reason or another. This fits the timeline reasonably well, but they did seem nervous about the deal even prior to the story coming out.

What Did We Learn? What Lessons Can Others Take Away?* Market Timing - as anyone who follows the stock market knows, the beginning of August was a rocky period. It appears to have stabilized more recently, but it could certainly be that, as in 2008 when funding suddenly dried up, the market's crashes took their toll on Neil's confidence or that of their firm's LPs (who said something like "don't make a capital call right now.")

* Something in the Research - it's also possible that something they found during their diligence into the market spooked them, but they couldn't or wouldn't share it with us. It's hard to imagine what it could be, or why they wouldn't tell us, but I suppose anything's possible.

I doubt we'll ever know for sure, and that's pretty frustrating. Last week, I sent the team this email:

The replies back were awesome. I won't share them here, but they killed whatever doubts I might have harbored from Neil's withdrawal. Working at SEOmoz just flat out rocks, and it's because I'm surrounded by some of the best people ever to be assembled. Re-reading those emails now still brings an unmitigated smile to my face.

The lessons from this process are challenging to compile, not only because it was such an inbound process, but because so much of the reasons for the final result are unknown. Nonetheless, I'll try:

* Don't Let Fundraising Distract You from What Really Matters - If I had this to do over again, a big part of me would still want to have the slower-than-expected growth in July to make sure we didn't get a fairweather friend who didn't really believe in the company onto the board, but I also know we could have been much more disciplined. Spending the team's time not just on phone calls and webinars to walk investors through our numbers, but time researching, pulling metrics, re-inforcing market questions, etc. was a waste. We should have let the investors do more of the work and kept the team more focused on the mission at hand. If an investor really wants to be part of Moz, a few missing, non-standard business metrics aren't going to change that.

* Inbound Interest is No Guarantee of Getting Funded - For some reason, I had this idea stuck in my head that if the company is being pitched to take funding by investors, the deal will be dramatically easier to do. This might be true, but "easier" doesn't mean "in the bag." Our first round did work largely this way - Michelle and Kelly pitched us, we said yes, money arrived. This time, Neil, Reggie, Todd and plenty of other reached out to us, pitched and at the end of the process, nada.

Our Plans Going Forward

Our Plans Going Forward* Be Careful About How & Where Funding is Communicated - We tried to be cautious this time around, not wanting to get our team or ourselves too excited before money was in the bank. Nevertheless, we definitely started planning ahead a bit prematurely. The nights and weekends (and a few days, too) spent brainstorming and roadmapping an SEOmoz with another $18mm in cash was time we certainly could have spent on more productive, realistic goals.

* Be Excellent to Everyone, All the Time - I can definitely confirm that the world of venture capital and private/growth equity is a very tiny one, and that entrepreneurs, partners and service providers talk incessantly and vociferously about nearly every experience with an investor or company. If you're in the startup world on any side of that equation, it pays to be a great human being and to treat everyone with respect (this is probably another full post worth writing at some point). We heard some not-so-great things about several potential investors, and it made us pull back pretty quickly. Folks in the Valley often talk about how "reputation is everything," and this experience re-inforced that for me.

* Never, Ever Get Cocky - I have to admit that sometime around the end of June/beginning of July, I was starting to feel pretty good. A bunch of investors wanted to put a LOT of money into our company. We were beating revenue month after month. We turned away investors instead of the other way around. I tried to stay humble, stay hungry and not get overly excited about things, but the idea of having liquidity for my family, the ability to grow Moz in a new and exciting way and, yeah, the idea of finally having some personal savings were all dancing in my head.

* Remember What Really Matters - No matter how this VC story went, I'm an incredibly lucky member of the human race. The big stuff is going amazingly well. My grandmother, who had a fall back in May, has almost entirely recovered. I'm surrounded by people I love to work with, all of whom are excited to come into the office every day, investment or no. And I'm married to her:

The best part about this otherwise frustrating result is that we didn't end up signing a deal with a firm who didn't truly believe in us, our market or our future. Despite our positive experiences with Neil from March - July, the last couple weeks clearly showed that he would have been a poor choice for our board of directors. Whatever caused the cold feet, it's better now than after the investment, when a wrong choice could have made life unpleasant for everyone for many years to come.

On the investment front - we've decided that attempting to raise a round of funding anytime in the next 6 months would be a mistake. We continue to receive calls from potential investors, but my message has shifted to "let's maybe talk again next year."

Personally, I feel burned. This is the second time in 3 years that I've gotten excited about raising a potential round of capital, and it turned out terribly both times. I'm not sure what I did wrong or what I should do differently next time. I also don't know how we could have done more diligence on Neil or his firm - literally everyone we talked to raved about him; even the skeptical third-parties who went digging into their mutual contacts for us had great things to say.

Phone calls and meetings are one thing, but this wasted a massive chunk of our time, energy and emotion. Putting faith in the process in the future would be hard - if a deal can fall through this late, when we weren't even pitching but got pitched... Well, I just don't know. Everything about this feels wrong.

What I can say is that this experience makes me and the rest of the Moz team even more inspired and motivated to build an amazing company. We can't help but feel passion for proving doubters and naysayers wrong. The greatest revenge is to execute like hell, bootstrap all the way, and do what we said we'd do - become Seattle's next billion-dollar startup, and make the world of marketing a better place.

I know we can do it.

p.s. A huge thank you to so many amazing people who helped us out with their advice, networks and reviews during this period - Mark Suster, Hugh Crean, Brian Halligan, Michelle Goldberg, Dharmesh Shah, Gautam Godhwani, Jason Cohen, Nirav Tolia, Kelly Smith, Dan Shapiro, Ben Huh - and many, many more. You were the best parts of this experience, and I hope I can repay the favor somehow in the future.

Sales/Marketing Investments Organic (Grow Free Traffic) Paid Acquisition (PPC, Behavioral, Social, etc) Branding (Make MozKnown + Trusted) Technology Investments Web Crawl (Grow Breadth + Freshness) Fresh Web (Compete w/ Google Alerts) Social Graph (Map the Major Networks) Product Investments Low Price Model ($25/month for lighter use) MozAlerts ($10/mthcompetitor to G Alerts) Classifying the Web (Employing Human Raters)

Potential Acquisitions

Why Mozis Uniquely Positioned to Win the Organic Market

#3: #4: #1: #2: Proven record of 2X+ growth for 4 years Unique, world-changing culture & attitude Passionate community of 300K+ marketers Our technology lead is very hard to catch

W e have a rare opportunity to become Seattle’s next $1 billion+ company, and we’d love to have you join us for the ride.