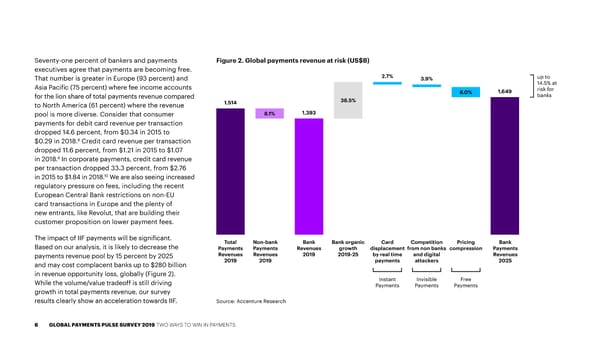

Seventy-one percent of bankers and payments Figure 2. Global payments revenue at risk (US$B) executives agree that payments are becoming free. That number is greater in Europe (93 percent) and 2.7% 3.9% up to Asia Pacific (75 percent) where fee income accounts 14.5% at 8.0% 1,649 risk for for the lion share of total payments revenue compared 38.5% banks to North America (61 percent) where the revenue 1,514 pool is more diverse. Consider that consumer 8.1% 1,393 payments for debit card revenue per transaction dropped 14.6 percent, from $0.34 in 2015 to 8 $0.29 in 2018. Credit card revenue per transaction dropped 11.6 percent, from $1.21 in 2015 to $1.07 9 in 2018. In corporate payments, credit card revenue per transaction dropped 33.3 percent, from $2.76 10 in 2015 to $1.84 in 2018. We are also seeing increased regulatory pressure on fees, including the recent European Central Bank restrictions on non-EU card transactions in Europe and the plenty of new entrants, like Revolut, that are building their customer proposition on lower payment fees. The impact of IIF payments will be significant. Total Non-bank Bank Bank organic Card Competition Pricing Bank Based on our analysis, it is likely to decrease the Payments Payments Revenues growth displacement from non banks compression Payments payments revenue pool by 15 percent by 2025 Revenues Revenues 2019 2019-25 by real time and digital Revenues and may cost complacent banks up to $280 billion 2019 2019 payments attackers 2025 in revenue opportunity loss, globally (Figure 2). While the volume/value tradeoff is still driving Instant Invisible Free Payments Payments Payments growth in total payments revenue, our survey results clearly show an acceleration towards IIF. Source: Accenture Research 6 GLOBAL PAYMENTS PULSE SURVEY 2019 TWO WAYS TO WIN IN PAYMENTS

Two Ways to Win in Payments Page 5 Page 7

Two Ways to Win in Payments Page 5 Page 7