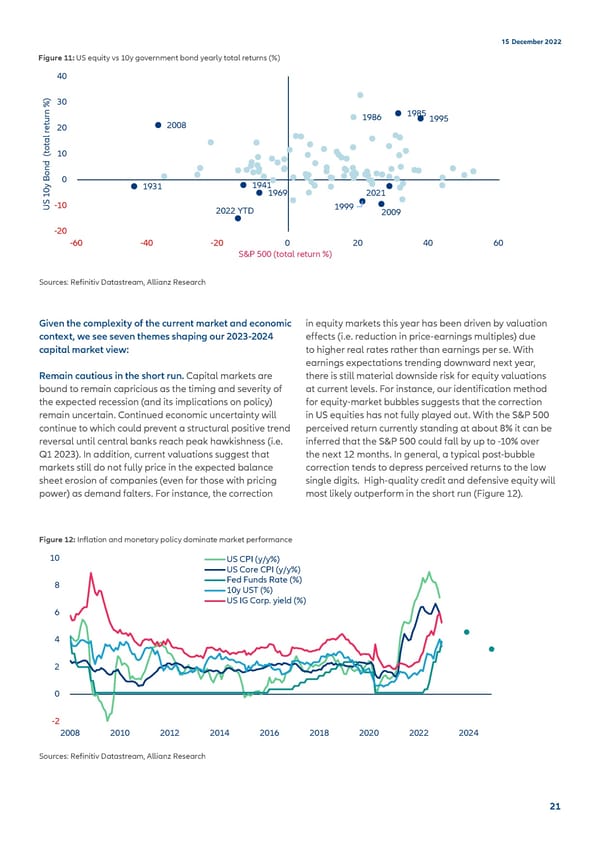

15 December 2022 Figure 11: US equity vs 10y government bond yearly total returns (%) 40 ) 30 % n 1985 r 1986 1995 u 2008 et20 r al t o t 10 ( d n Bo 0 1931 1941 10y 1969 2021 S-10 1999 U 2022 YTD 2009 -20 -60 -40 -20 0 20 40 60 S&P 500 (total return %) Sources: Refinitiv Datastream, Allianz Research Given the complexity of the current market and economic in equity markets this year has been driven by valuation context, we see seven themes shaping our 2023-2024 effects (i.e. reduction in price-earnings multiples) due capital market view: to higher real rates rather than earnings per se. With earnings expectations trending downward next year, Capital MarketsRemain cautious in the short run. Capital markets are there is still material downside risk for equity valuations bound to remain capricious as the timing and severity of at current levels. For instance, our identification method the expected recession (and its implications on policy) for equity-market bubbles suggests that the correction remain uncertain. Continued economic uncertainty will in US equities has not fully played out. With the S&P 500 continue to which could prevent a structural positive trend perceived return currently standing at about 8% it can be reversal until central banks reach peak hawkishness (i.e. inferred that the S&P 500 could fall by up to -10% over Q1 2023). In addition, current valuations suggest that the next 12 months. In general, a typical post-bubble markets still do not fully price in the expected balance correction tends to depress perceived returns to the low sheet erosion of companies (even for those with pricing single digits. High-quality credit and defensive equity will power) as demand falters. For instance, the correction most likely outperform in the short run (Figure 12). Figure 12: Inflation and monetary policy dominate market performance 10 US CPI (y/y%) US Core CPI (y/y%) 8 Fed Funds Rate (%) 10y UST (%) US IG Corp. yield (%) 6 4 2 0 -2 2008 2010 2012 2014 2016 2018 2020 2022 2024 Sources: Refinitiv Datastream, Allianz Research 21

Allianz 2022 Outlook final Page 20 Page 22

Allianz 2022 Outlook final Page 20 Page 22