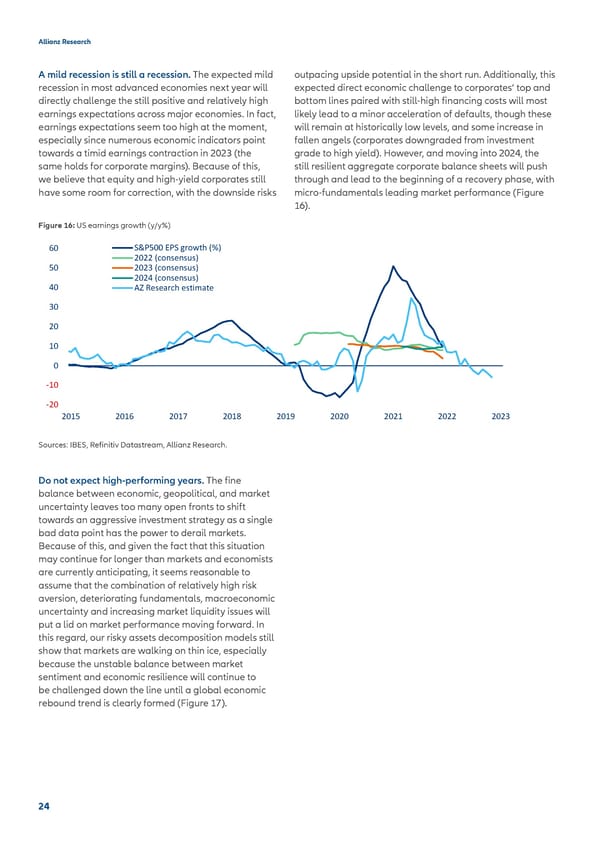

Allianz Research A mild recession is still a recession. The expected mild outpacing upside potential in the short run. Additionally, this recession in most advanced economies next year will expected direct economic challenge to corporates’ top and directly challenge the still positive and relatively high bottom lines paired with still-high financing costs will most earnings expectations across major economies. In fact, likely lead to a minor acceleration of defaults, though these earnings expectations seem too high at the moment, will remain at historically low levels, and some increase in especially since numerous economic indicators point fallen angels (corporates downgraded from investment towards a timid earnings contraction in 2023 (the grade to high yield). However, and moving into 2024, the same holds for corporate margins). Because of this, still resilient aggregate corporate balance sheets will push we believe that equity and high-yield corporates still through and lead to the beginning of a recovery phase, with have some room for correction, with the downside risks micro-fundamentals leading market performance (Figure 16). Figure 16: US earnings growth (y/y%) 60 S&P500 EPS growth (%) 2022 (consensus) 50 2023 (consensus) 2024 (consensus) 40 AZ Research estimate 30 20 10 0 -10 -20 2015 2016 2017 2018 2019 2020 2021 2022 2023 Sources: IBES, Refinitiv Datastream, Allianz Research. Do not expect high-performing years. The fine balance between economic, geopolitical, and market uncertainty leaves too many open fronts to shift towards an aggressive investment strategy as a single bad data point has the power to derail markets. Because of this, and given the fact that this situation may continue for longer than markets and economists are currently anticipating, it seems reasonable to assume that the combination of relatively high risk aversion, deteriorating fundamentals, macroeconomic uncertainty and increasing market liquidity issues will put a lid on market performance moving forward. In this regard, our risky assets decomposition models still show that markets are walking on thin ice, especially because the unstable balance between market sentiment and economic resilience will continue to be challenged down the line until a global economic rebound trend is clearly formed (Figure 17). 24

Allianz 2022 Outlook final Page 23 Page 25

Allianz 2022 Outlook final Page 23 Page 25