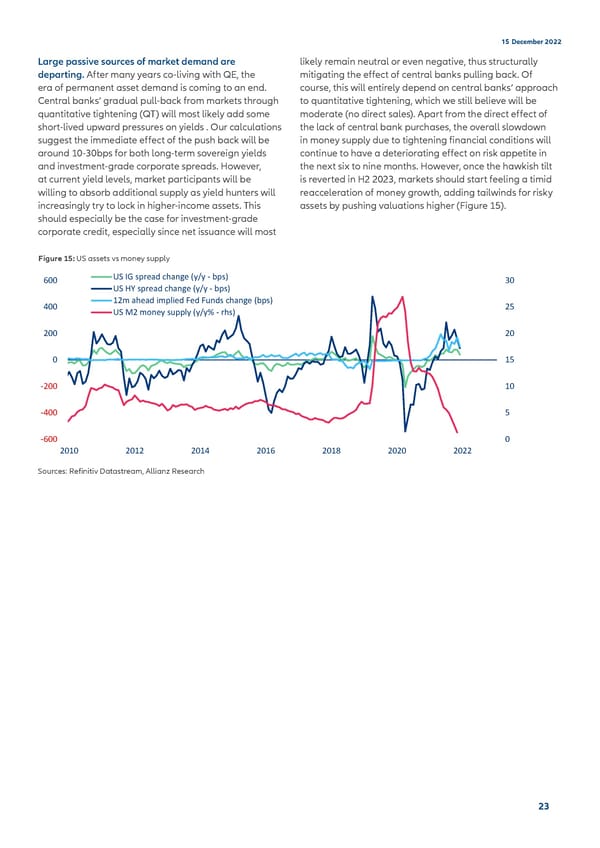

15 December 2022 Large passive sources of market demand are likely remain neutral or even negative, thus structurally departing. After many years co-living with QE, the mitigating the effect of central banks pulling back. Of era of permanent asset demand is coming to an end. course, this will entirely depend on central banks’ approach Central banks’ gradual pull-back from markets through to quantitative tightening, which we still believe will be quantitative tightening (QT) will most likely add some moderate (no direct sales). Apart from the direct effect of short-lived upward pressures on yields . Our calculations the lack of central bank purchases, the overall slowdown suggest the immediate effect of the push back will be in money supply due to tightening financial conditions will around 10-30bps for both long-term sovereign yields continue to have a deteriorating effect on risk appetite in and investment-grade corporate spreads. However, the next six to nine months. However, once the hawkish tilt at current yield levels, market participants will be is reverted in H2 2023, markets should start feeling a timid willing to absorb additional supply as yield hunters will reacceleration of money growth, adding tailwinds for risky increasingly try to lock in higher-income assets. This assets by pushing valuations higher (Figure 15). should especially be the case for investment-grade corporate credit, especially since net issuance will most Figure 15: US assets vs money supply 600 US IG spread change (y/y - bps) 30 US HY spread change (y/y - bps) 400 12m ahead implied Fed Funds change (bps) 25 US M2 money supply (y/y% - rhs) 200 20 0 15 -200 10 -400 5 -600 0 2010 2012 2014 2016 2018 2020 2022 Sources: Refinitiv Datastream, Allianz Research 23

Allianz 2022 Outlook final Page 22 Page 24

Allianz 2022 Outlook final Page 22 Page 24