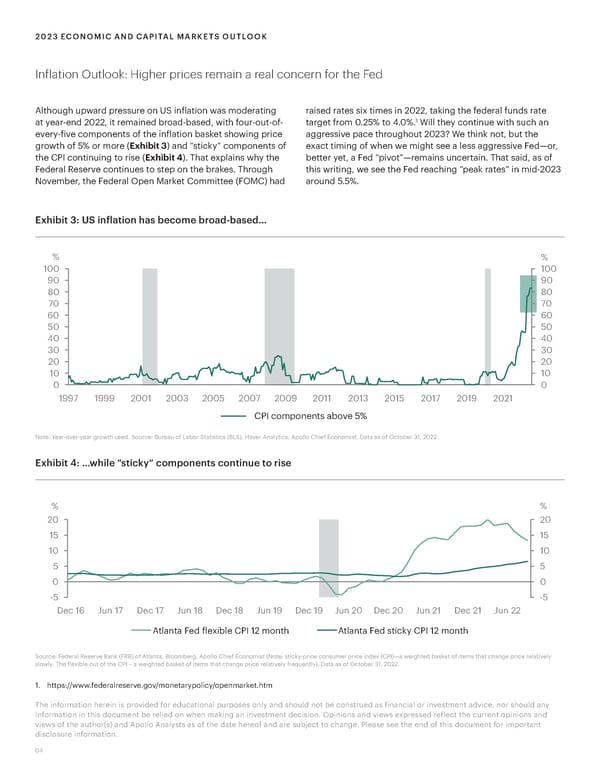

2023 ECONOMIC AND CAPITAL MARKETS OUTLOOK Inflation Outlook: Higher prices remain a real concern for the Fed Although upward pressure on US inflation was moderating raised rates six times in 2022, taking the federal funds rate 1 at year-end 2022, it remained broad-based, with four-out-of- target from 0.25% to 4.0%. Will they continue with such an every-five components of the inflation basket showing price aggressive pace throughout 2023? We think not, but the growth of 5% or more (Exhibit 3) and “sticky” components of exact timing of when we might see a less aggressive Fed—or, the CPI continuing to rise (Exhibit 4). That explains why the better yet, a Fed “pivot”—remains uncertain. That said, as of Federal Reserve continues to step on the brakes. Through this writing, we see the Fed reaching “peak rates” in mid-2023 November, the Federal Open Market Committee (FOMC) had around 5.5%. Exhibit 3: US inflation has become broad-based… % % 100 100 90 90 80 80 70 70 60 60 50 50 40 40 30 30 20 20 10 10 0 0 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 CPI components above 5% Note: Year-over-year growth used. Source: Bureau of Labor Statistics (BLS), Haver Analytics, Apollo Chief Economist. Data as of October 31, 2022. Exhibit 4: …while “sticky” components continue to rise % % 20 20 15 15 10 10 5 5 0 0 -5 -5 Dec 16 Jun 17 Dec 17 Jun 18 Dec 18 Jun 19 Dec 19 Jun 20 Dec 20 Jun 21 Dec 21 Jun 22 Atlanta Fed flexible CPI 12 mnt Atlanta Fed tic CPI 12 mnt Source: Federal Reserve Bank (FRB) of Atlanta, Bloomberg, Apollo Chief Economist (Note: sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly; The flexible cut of the CPI – a weighted basket of items that change price relatively frequently). Data as of October 31, 2022. 1. https://www.federalreserve.gov/monetarypolicy/openmarket.htm The information herein is provided for educational purposes only and should not be construed as financial or investment advice, nor should any information in this document be relied on when making an investment decision. Opinions and views expressed reflect the current opinions and views of the author(s) and Apollo Analysts as of the date hereof and are subject to change. Please see the end of this document for important disclosure information. 04

Apollo 2023 Economic and Capital Markets Outlook Page 3 Page 5

Apollo 2023 Economic and Capital Markets Outlook Page 3 Page 5