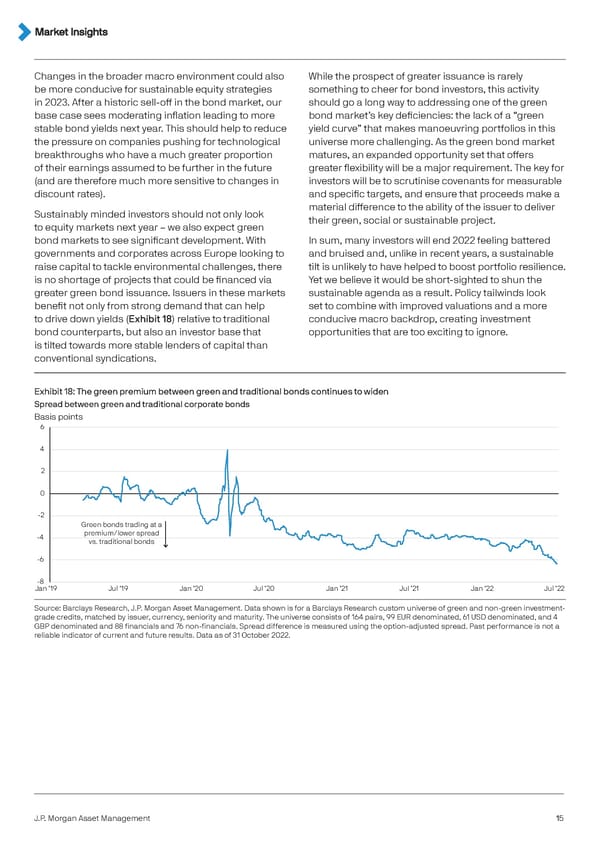

Changes in the broader macro environment could also While the prospect of greater issuance is rarely be more conducive for sustainable equity strategies something to cheer for bond investors, this activity in 2023. After a historic sell-off in the bond market, our should go a long way to addressing one of the green base case sees moderating inflation leading to more bond market’s key deficiencies: the lack of a “green stable bond yields next year. This should help to reduce yield curve” that makes manoeuvring portfolios in this the pressure on companies pushing for technological universe more challenging. As the green bond market breakthroughs who have a much greater proportion matures, an expanded opportunity set that offers of their earnings assumed to be further in the future greater flexibility will be a major requirement. The key for (and are therefore much more sensitive to changes in investors will be to scrutinise covenants for measurable discount rates). and specific targets, and ensure that proceeds make a Sustainably minded investors should not only look material difference to the ability of the issuer to deliver to equity markets next year – we also expect green their green, social or sustainable project. bond markets to see significant development. With In sum, many investors will end 2022 feeling battered governments and corporates across Europe looking to and bruised and, unlike in recent years, a sustainable raise capital to tackle environmental challenges, there tilt is unlikely to have helped to boost portfolio resilience. is no shortage of projects that could be financed via Yet we believe it would be short-sighted to shun the greater green bond issuance. Issuers in these markets sustainable agenda as a result. Policy tailwinds look benefit not only from strong demand that can help set to combine with improved valuations and a more to drive down yields (Exhibit 18) relative to traditional conducive macro backdrop, creating investment bond counterparts, but also an investor base that opportunities that are too exciting to ignore. is tilted towards more stable lenders of capital than conventional syndications. Exhibit 18: The green premium between green and traditional bonds continues to widen Spread between green and traditional corporate bonds Basis points 6 4 2 0 -2 Green bonds trading at a -4 premium/lower spread vs. traditional bonds -6 -8 Jan ’19 Jul ’19 Jan ’20 Jul ’20 Jan ’21 Jul ’21 Jan ’22 Jul ’22 Source: Barclays Research, J.P. Morgan Asset Management. Data shown is for a Barclays Research custom universe of green and non-green investment- grade credits, matched by issuer, currency, seniority and maturity. The universe consists of 164 pairs, 99 EUR denominated, 61 USD denominated, and 4 GBP denominated and 88 financials and 76 non-financials. Spread difference is measured using the option-adjusted spread. Past performance is not a reliable indicator of current and future results. Data as of 31 October 2022. J.P. Morgan Asset Management 15

J.P. Morgan Investment Outlook 2023 Page 14 Page 16

J.P. Morgan Investment Outlook 2023 Page 14 Page 16