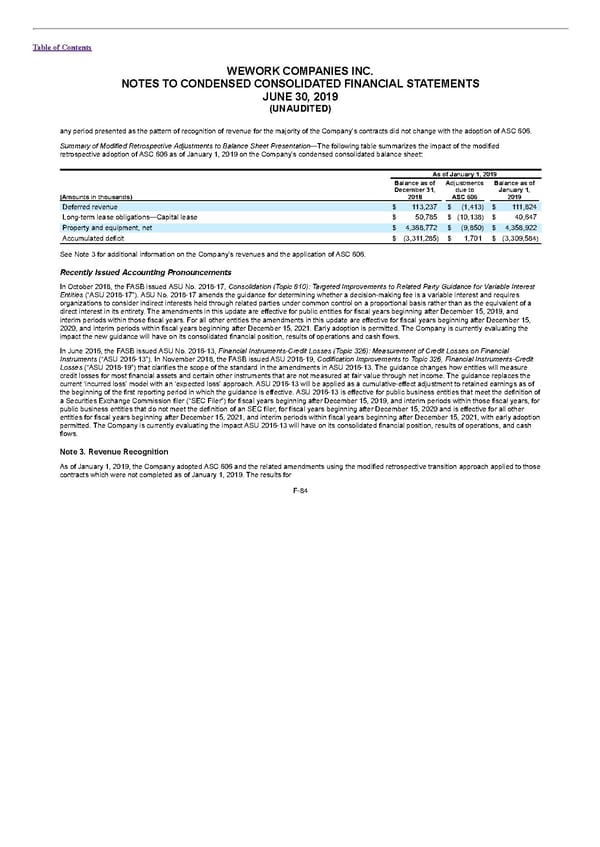

Table of Contents WEWORK COMPANIES INC. NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS JUNE 30, 2019 (UNAUDITED) any period presented as the pattern of recognition of revenue for the majority of the Company’s contracts did not change with the adoption of ASC 606. Summary of Modified Retrospective Adjustments to Balance Sheet Presentation—The following table summarizes the impact of the modified retrospective adoption of ASC 606 as of January 1, 2019 on the Company’s condensed consolidated balance sheet: As of January 1, 2019 Balance as of Adjustments Balance as of December 31, due to January 1, (Amounts in thousands) 2018 ASC 606 2019 Deferred revenue $ 113,237 $ (1,413) $ 111,824 Long-term lease obligations—Capital lease $ 50,785 $ (10,138) $ 40,647 Property and equipment, net $ 4,368,772 $ (9,850) $ 4,358,922 Accumulated deficit $ (3,311,285) $ 1,701 $ (3,309,584) See Note 3 for additional information on the Company’s revenues and the application of ASC 606. Recently Issued Accounting Pronouncements In October 2018, the FASB issued ASU No. 2018-17, Consolidation (Topic 810): Targeted Improvements to Related Party Guidance for Variable Interest Entities (“ASU 2018-17”). ASU No. 2018-17 amends the guidance for determining whether a decision-making fee is a variable interest and requires organizations to consider indirect interests held through related parties under common control on a proportional basis rather than as the equivalent of a direct interest in its entirety. The amendments in this update are effective for public entities for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. For all other entities the amendments in this update are effective for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021. Early adoption is permitted. The Company is currently evaluating the impact the new guidance will have on its consolidated financial position, results of operations and cash flows. In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (“ASU 2016-13”). In November 2018, the FASB issued ASU 2018-19, Codification Improvements to Topic 326, Financial Instruments-Credit Losses (“ASU 2018-19”) that clarifies the scope of the standard in the amendments in ASU 2016-13. The guidance changes how entities will measure credit losses for most financial assets and certain other instruments that are not measured at fair value through net income. The guidance replaces the current ‘incurred loss’ model with an ‘expected loss’ approach. ASU 2016-13 will be applied as a cumulative-effect adjustment to retained earnings as of the beginning of the first reporting period in which the guidance is effective. ASU 2016-13 is effective for public business entities that meet the definition of a Securities Exchange Commission filer (“SEC Filer”) for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years, for public business entities that do not meet the definition of an SEC filer, for fiscal years beginning after December 15, 2020 and is effective for all other entities for fiscal years beginning after December 15, 2021, and interim periods within fiscal years beginning after December 15, 2021, with early adoption permitted. The Company is currently evaluating the impact ASU 2016-13 will have on its consolidated financial position, results of operations, and cash flows. Note 3. Revenue Recognition As of January 1, 2019, the Company adopted ASC 606 and the related amendments using the modified retrospective transition approach applied to those contracts which were not completed as of January 1, 2019. The results for F-84

S1 - WeWork Prospectus Page 327 Page 329

S1 - WeWork Prospectus Page 327 Page 329