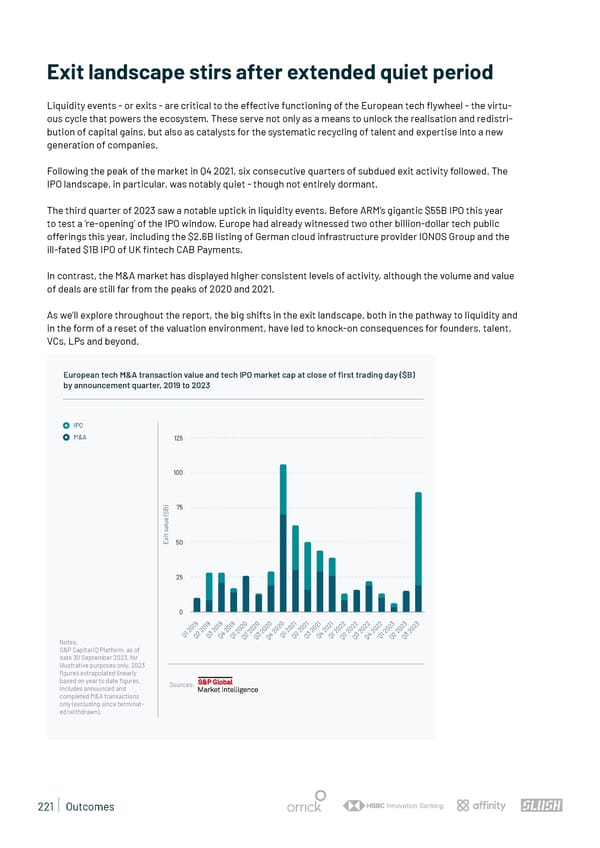

Exit landscape stirs after extended quiet period Liquidity events - or exits - are critical to the effective functioning of the European tech 昀氀ywheel - the virtu- ous cycle that powers the ecosystem. These serve not only as a means to unlock the realisation and redistri- bution of capital gains, but also as catalysts for the systematic recycling of talent and expertise into a new generation of companies. Following the peak of the market in Q4 2021, six consecutive quarters of subdued exit activity followed. The IPO landscape, in particular, was notably quiet - though not entirely dormant. The third quarter of 2023 saw a notable uptick in liquidity events. Before ARM’s gigantic $55B IPO this year to test a ‘re-opening’ of the IPO window, Europe had already witnessed two other billion-dollar tech public offerings this year, including the $2.6B listing of German cloud infrastructure provider IONOS Group and the ill-fated $1B IPO of UK 昀椀ntech CAB Payments. In contrast, the M&A market has displayed higher consistent levels of activity, although the volume and value of deals are still far from the peaks of 2020 and 2021. As we’ll explore throughout the report, the big shifts in the exit landscape, both in the pathway to liquidity and in the form of a reset of the valuation environment, have led to knock-on consequences for founders, talent, VCs, LPs and beyond. European tech M&A transaction value and tech IPO market cap at close of first trading day ($B) by announcement quarter, 2019 to 2023 IPO M&A 125 100 ) 75 B $ ( e u l a v t i x E 50 25 0 9 9 9 9 0 0 0 0 1 1 1 1 2 2 2 2 3 3 3 1 1 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 20 20 20 20 0 0 0 0 20 20 20 20 0 0 0 0 0 0 0 2 2 2 2 2 2 2 2 2 2 2 1 2 3 4 1 2 3 4 1 1 Q Q Q Q Q1 2 3 4 Q Q Q Q Q 2 3 4 Q 2 3 Notes: Q Q Q Q Q Q Q Q S&P Capital IQ Platform, as of date 30 September 2023, for illustrative purposes only. 2023 figures extrapolated linearly based on year to date figures. Sources: Includes announced and completed M&A transactions only (excluding since terminat- ed/withdrawn). 221 | Outcomes

State of European Tech | 2023 Page 220 Page 222

State of European Tech | 2023 Page 220 Page 222