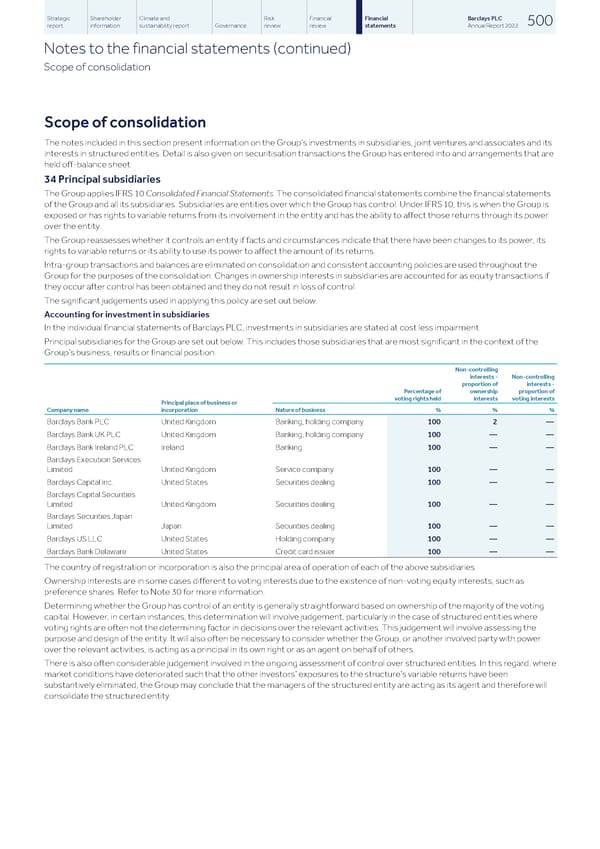

Strategic Shareholder Climate and Risk Financial Financial Barclays PLC 500 report information sustainability report Governance review review statements Annual Report 2022 Notes to the financial statements (continued) Scope of consolidation Scope of consolidation The notes included in this section present information on the Group’s investments in subsidiaries, joint ventures and associates and its interests in structured entities. Detail is also given on securitisation transactions the Group has entered into and arrangements that are held off-balance sheet. 34 Principal subsidiaries The Group applies IFRS 10 Consolidated Financial Statements. The consolidated financial statements combine the financial statements of the Group and all its subsidiaries. Subsidiaries are entities over which the Group has control. Under IFRS 10, this is when the Group is exposed or has rights to variable returns from its involvement in the entity and has the ability to affect those returns through its power over the entity. The Group reassesses whether it controls an entity if facts and circumstances indicate that there have been changes to its power, its rights to variable returns or its ability to use its power to affect the amount of its returns. Intra-group transactions and balances are eliminated on consolidation and consistent accounting policies are used throughout the Group for the purposes of the consolidation. Changes in ownership interests in subsidiaries are accounted for as equity transactions if they occur after control has been obtained and they do not result in loss of control. The significant judgements used in applying this policy are set out below. Accounting for investment in subsidiaries In the individual financial statements of Barclays PLC, investments in subsidiaries are stated at cost less impairment. Principal subsidiaries for the Group are set out below. This includes those subsidiaries that are most significant in the context of the Group’s business, results or financial position. Non-controlling interests - Non-controlling proportion of interests - Percentage of ownership proportion of voting rights held interests voting interests Principal place of business or Company name incorporation Nature of business % % % Barclays Bank PLC United Kingdom Banking, holding company 100 2 — Barclays Bank UK PLC United Kingdom Banking, holding company 100 — — Barclays Bank Ireland PLC Ireland Banking 100 — — Barclays Execution Services Limited United Kingdom Service company 100 — — Barclays Capital Inc. United States Securities dealing 100 — — Barclays Capital Securities Limited United Kingdom Securities dealing 100 — — Barclays Securities Japan Limited Japan Securities dealing 100 — — Barclays US LLC United States Holding company 100 — — Barclays Bank Delaware United States Credit card issuer 100 — — The country of registration or incorporation is also the principal area of operation of each of the above subsidiaries. Ownership interests are in some cases different to voting interests due to the existence of non-voting equity interests, such as preference shares. Refer to Note 30 for more information. Determining whether the Group has control of an entity is generally straightforward based on ownership of the majority of the voting capital. However, in certain instances, this determination will involve judgement, particularly in the case of structured entities where voting rights are often not the determining factor in decisions over the relevant activities. This judgement will involve assessing the purpose and design of the entity. It will also often be necessary to consider whether the Group, or another involved party with power over the relevant activities, is acting as a principal in its own right or as an agent on behalf of others. There is also often considerable judgement involved in the ongoing assessment of control over structured entities. In this regard, where market conditions have deteriorated such that the other investors’ exposures to the structure’s variable returns have been substantively eliminated, the Group may conclude that the managers of the structured entity are acting as its agent and therefore will consolidate the structured entity.

Barclays PLC - Annual Report - 2022 Page 501 Page 503

Barclays PLC - Annual Report - 2022 Page 501 Page 503