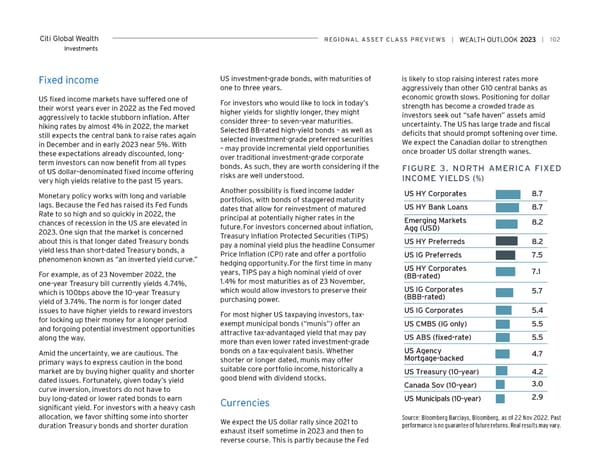

Citi Global Wealth reGioNAL ASSeT CLASS PreviewS | | 102 Investments Fixed income US investment-grade bonds, with maturities of is likely to stop raising interest rates more one to three years. aggressively than other G10 central banks as US fixed income markets have suffered one of economic growth slows. Positioning for dollar their worst years ever in 2022 as the Fed moved For investors who would like to lock in today’s strength has become a crowded trade as aggressively to tackle stubborn inflation. After higher yields for slightly longer, they might investors seek out “safe haven” assets amid hiking rates by almost 4% in 2022, the market consider three- to seven-year maturities. uncertainty. The US has large trade and fiscal still expects the central bank to raise rates again Selected BB-rated high-yield bonds – as well as deficits that should prompt softening over time. in December and in early 2023 near 5%. With selected investment-grade preferred securities We expect the Canadian dollar to strengthen these expectations already discounted, long- – may provide incremental yield opportunities once broader US dollar strength wanes. term investors can now benefit from all types over traditional investment-grade corporate of US dollar–denominated fixed income offering bonds. As such, they are worth considering if the FiGUre 3. NorTH AMeriCA FiXeD very high yields relative to the past 15 years. risks are well understood. iNCoMe YieLDS (%) Monetary policy works with long and variable Another possibility is fixed income ladder US HY Corporates 8.7 lags. Because the Fed has raised its Fed Funds portfolios, with bonds of staggered maturity dates that allow for reinvestment of matured US HY Bank Loans 8.7 Rate to so high and so quickly in 2022, the principal at potentially higher rates in the chances of recession in the US are elevated in Emerging Markets 8.2 2023. One sign that the market is concerned future. For investors concerned about inflation, Agg (USD) about this is that longer dated Treasury bonds Treasury Inflation Protected Securities (TIPS) US HY Preferreds 8.2 yield less than short-dated Treasury bonds, a pay a nominal yield plus the headline Consumer phenomenon known as “an inverted yield curve.” Price Inflation (CPI) rate and offer a portfolio US IG Preferreds 7.5 hedging opportunity. For the first time in many US HY Corporates For example, as of 23 November 2022, the years, TIPS pay a high nominal yield of over (BB-rated) 7.1 one-year Treasury bill currently yields 4.74%, 1.4% for most maturities as of 23 November, which is 100bps above the 10-year Treasury which would allow investors to preserve their US IG Corporates 5.7 yield of 3.74%. The norm is for longer dated purchasing power. (BBB-rated) issues to have higher yields to reward investors For most higher US taxpaying investors, tax- US IG Corporates 5.4 for locking up their money for a longer period exempt municipal bonds (“munis”) offer an US CMBS (IG only) 5.5 and forgoing potential investment opportunities attractive tax-advantaged yield that may pay along the way. more than even lower rated investment-grade US ABS (fixed-rate) 5.5 Amid the uncertainty, we are cautious. The bonds on a tax-equivalent basis. Whether US Agency 4.7 primary ways to express caution in the bond shorter or longer dated, munis may offer Mortgage-backed market are by buying higher quality and shorter suitable core portfolio income, historically a US Treasury (10-year) 4.2 dated issues. Fortunately, given today’s yield good blend with dividend stocks. 3.0 curve inversion, investors do not have to Canada Sov (10-year) buy long-dated or lower rated bonds to earn Currencies US Municipals (10-year) 2.9 significant yield. For investors with a heavy cash allocation, we favor shifting some into shorter We expect the US dollar rally since 2021 to Source: Bloomberg Barclays, Bloomberg, as of 22 Nov 2022. Past duration Treasury bonds and shorter duration exhaust itself sometime in 2023 and then to performance is no guarantee of future returns. Real results may vary. reverse course. This is partly because the Fed

Citi Wealth Outlook 2023 Page 101 Page 103

Citi Wealth Outlook 2023 Page 101 Page 103