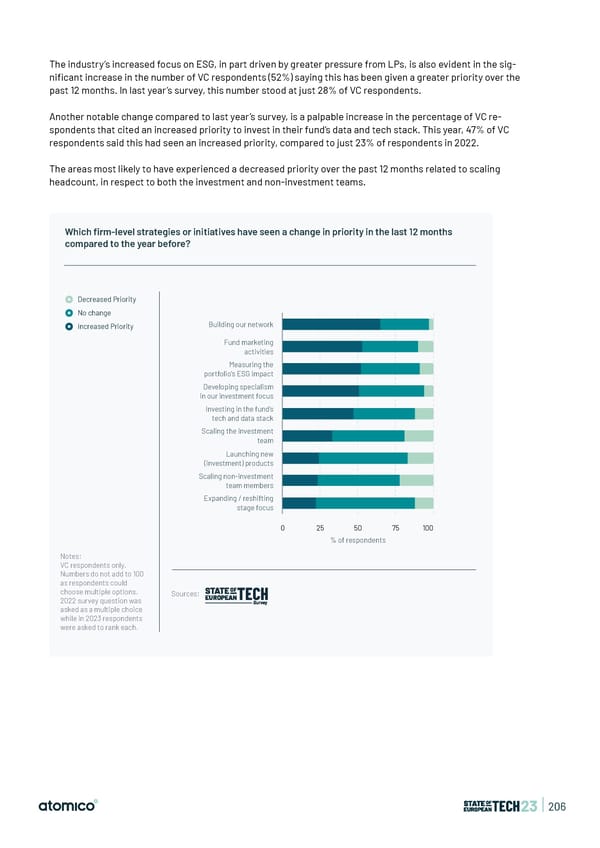

The industry’s increased focus on ESG, in part driven by greater pressure from LPs, is also evident in the sig- ni昀椀cant increase in the number of VC respondents (52%) saying this has been given a greater priority over the past 12 months. In last year’s survey, this number stood at just 28% of VC respondents. Another notable change compared to last year’s survey, is a palpable increase in the percentage of VC re- spondents that cited an increased priority to invest in their fund’s data and tech stack. This year, 47% of VC respondents said this had seen an increased priority, compared to just 23% of respondents in 2022. The areas most likely to have experienced a decreased priority over the past 12 months related to scaling headcount, in respect to both the investment and non-investment teams. Which firm-level strategies or initiatives have seen a change in priority in the last 12 months compared to the year before? Decreased Priority No change Increased Priority Building our network Fund marketing activities Measuring the portfolio's ESG impact Developing specialism in our investment focus Investing in the fund’s tech and data stack Scaling the investment team Launching new (investment) products Scaling non-investment team members Expanding / reshifting stage focus 0 25 50 75 100 % of respondents Notes: VC respondents only. Numbers do not add to 100 as respondents could choose multiple options. Sources: 2022 survey question was asked as a multiple choice while in 2023 respondents were asked to rank each. | 206

State of European Tech | 2023 Page 205 Page 207

State of European Tech | 2023 Page 205 Page 207