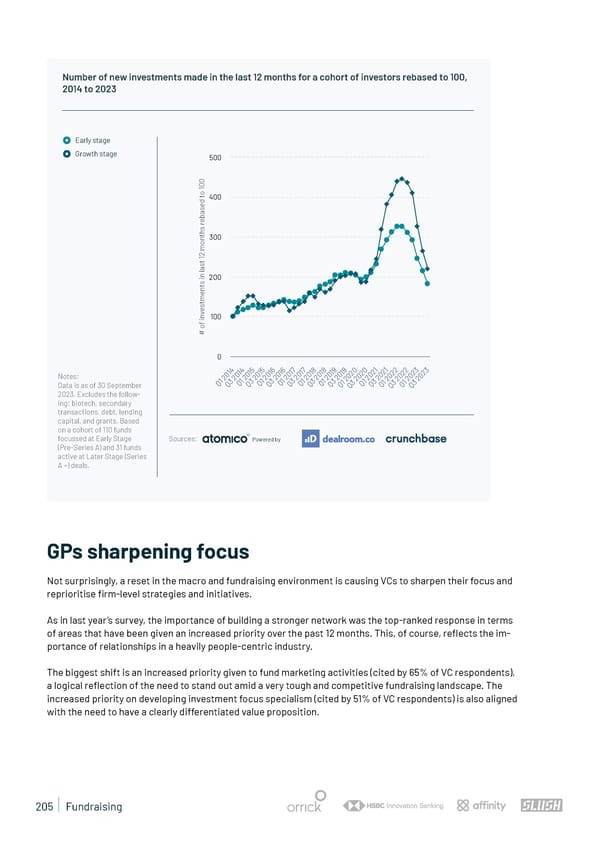

Number of new investments made in the last 12 months for a cohort of investors rebased to 100, 2014 to 2023 Early stage Growth stage 500 0 0 1 o t 400 d e s a b e r s h t300 n o m 2 1 t s a l n i200 s t n e m t s e v n 100 i f o # 0 4 4 5 5 6 6 17 17 8 8 9 9 0 0 1 1 2 2 3 3 1 1 1 1 1 1 0 0 1 1 1 1 2 2 2 2 2 2 2 2 Notes: 0 0 0 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 0 0 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 1 3 1 3 1 3 1 3 1 3 1 3 1 3 1 Q Q Q Q Q Q Q Q Q Q Q Q 1 3 Q Q 1 3 Q 3 Data is as of 30 September Q Q Q Q Q 2023. Excludes the follow- ing: biotech, secondary transactions, debt, lending capital, and grants. Based on a cohort of 110 funds focussed at Early Stage Sources: Powered by (Pre-Series A) and 31 funds active at Later Stage (Series A +) deals. GPs sharpening focus Not surprisingly, a reset in the macro and fundraising environment is causing VCs to sharpen their focus and reprioritise 昀椀rm-level strategies and initiatives. As in last year’s survey, the importance of building a stronger network was the top-ranked response in terms of areas that have been given an increased priority over the past 12 months. This, of course, re昀氀ects the im- portance of relationships in a heavily people-centric industry. The biggest shift is an increased priority given to fund marketing activities (cited by 65% of VC respondents), a logical re昀氀ection of the need to stand out amid a very tough and competitive fundraising landscape. The increased priority on developing investment focus specialism (cited by 51% of VC respondents) is also aligned with the need to have a clearly differentiated value proposition. 205 | Fundraising

State of European Tech | 2023 Page 204 Page 206

State of European Tech | 2023 Page 204 Page 206