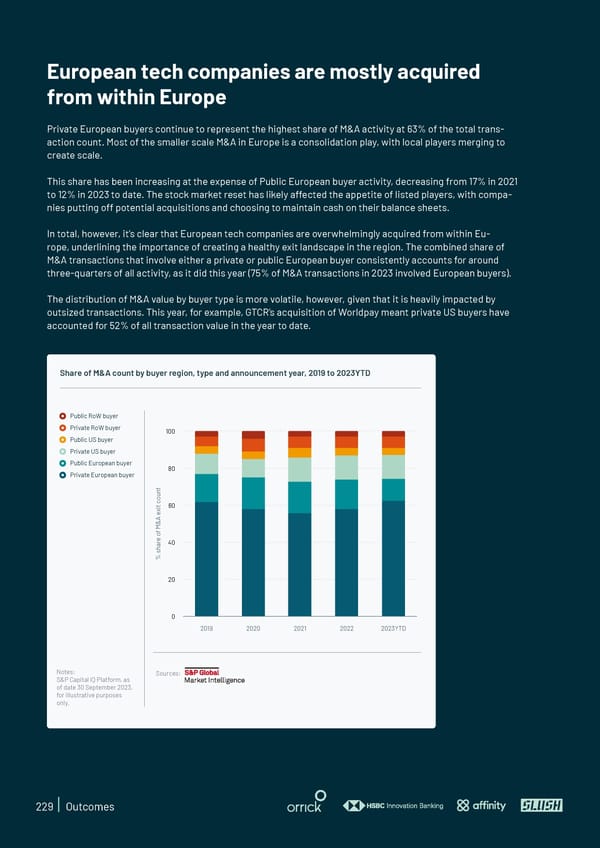

European tech companies are mostly acquired from within Europe Private European buyers continue to represent the highest share of M&A activity at 63% of the total trans- action count. Most of the smaller scale M&A in Europe is a consolidation play, with local players merging to create scale. This share has been increasing at the expense of Public European buyer activity, decreasing from 17% in 2021 to 12% in 2023 to date. The stock market reset has likely affected the appetite of listed players, with compa- nies putting off potential acquisitions and choosing to maintain cash on their balance sheets. In total, however, it’s clear that European tech companies are overwhelmingly acquired from within Eu- rope, underlining the importance of creating a healthy exit landscape in the region. The combined share of M&A transactions that involve either a private or public European buyer consistently accounts for around three-quarters of all activity, as it did this year (75% of M&A transactions in 2023 involved European buyers). The distribution of M&A value by buyer type is more volatile, however, given that it is heavily impacted by outsized transactions. This year, for example, GTCR’s acquisition of Worldpay meant private US buyers have accounted for 52% of all transaction value in the year to date. Share of M&A count by buyer region, type and announcement year, 2019 to 2023YTD Public RoW buyer Private RoW buyer 100 Public US buyer Private US buyer Public European buyer 80 Private European buyer t n u o c t 60 i x e A & M f o e r 40 a h s % 20 0 2019 2020 2021 2022 2023YTD Notes: Sources: S&P Capital IQ Platform, as of date 30 September 2023, for illustrative purposes only. 229 | Outcomes

State of European Tech | 2023 Page 228 Page 230

State of European Tech | 2023 Page 228 Page 230