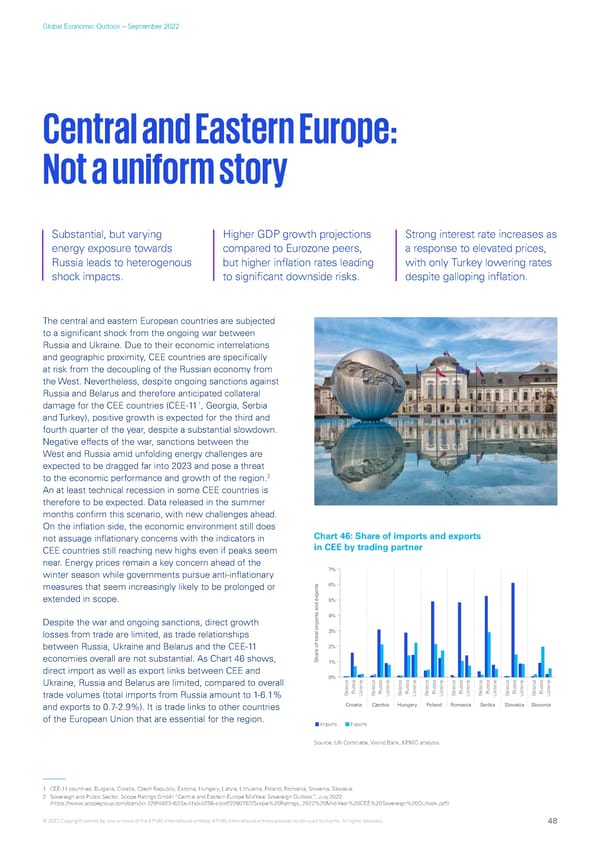

Global Economic Outlook – September 2022 Central and Eastern Europe: Not a uniform story Substantial, but varying Higher GDP growth projections Strong interest rate increases as energy exposure towards compared to Eurozone peers, a response to elevated prices, Russia leads to heterogenous but higher inflation rates leading with only Turkey lowering rates shock impacts. to significant downside risks. despite galloping inflation. The central and eastern European countries are subjected to a significant shock from the ongoing war between Russia and Ukraine. Due to their economic interrelations and geographic proximity, CEE countries are specifically at risk from the decoupling of the Russian economy from the West. Nevertheless, despite ongoing sanctions against Russia and Belarus and therefore anticipated collateral 1 damage for the CEE countries (CEE-11 , Georgia, Serbia and Turkey), positive growth is expected for the third and fourth quarter of the year, despite a substantial slowdown. Negative effects of the war, sanctions between the West and Russia amid unfolding energy challenges are expected to be dragged far into 2023 and pose a threat 2 to the economic performance and growth of the region. An at least technical recession in some CEE countries is therefore to be expected. Data released in the summer months confirm this scenario, with new challenges ahead. On the inflation side, the economic environment still does not assuage inflationary concerns with the indicators in Chart 46: Share of imports and exports CEE countries still reaching new highs even if peaks seem in CEE by trading partner near. Energy prices remain a key concern ahead of the winter season while governments pursue anti-inflationary 7% measures that seem increasingly likely to be prolonged or ts 6% extended in scope. 5% ts and expor4% Despite the war and ongoing sanctions, direct growth losses from trade are limited, as trade relationships 3% between Russia, Ukraine and Belarus and the CEE-11 2% economies overall are not substantial. As Chart 46 shows, Share of total impor1% direct import as well as export links between CEE and 0% Ukraine, Russia and Belarus are limited, compared to overall us us us us us us us us elarussia elarussia elarussia elarussia elarussia elarussia elarussia elarussia trade volumes (total imports from Russia amount to 1-6.1% B R UkraineBR UkraineB R UkraineBR UkraineB R UkraineBR UkraineB R UkraineBR Ukraine and exports to 0.7-2.9%). It is trade links to other countries Croatia Czechia Hungary Poland Romania Serbia Slovakia Slovenia of the European Union that are essential for the region. Imports Exports Source: UN Comtrade, World Bank, KPMG analysis. 1 CEE-11 countries: Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovenia, Slovakia. 2 Sovereign and Public Sector, Scope Ratings GmbH “Central and Eastern Europe MidYear Sovereign Outlook”, July 2022 (https://www.scopegroup.com/dam/jcr:129f4653-633a-41ab-b756-c4cdf2260787/Scope%20Ratings_2022%20Mid-Year%20CEE%20Sovereign%20Outlook.pdf) © 2022 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved. 48

KPMG Global Economic Outlook - H2 2022 report Page 47 Page 49

KPMG Global Economic Outlook - H2 2022 report Page 47 Page 49